Social Security Credits for Family Caregivers: What You Are and Are Not Earning Right Now

Unpaid family caregiving builds zero Social Security credits, because the work generates no reported income and the Social Security Administration has no record it ever happened. Every year spent caregiving without pay enters your benefit calculation as a zero, pulling down the 35-year earnings average that determines your monthly retirement check. When a family caregiver gets paid through a Medicaid program and that income is reported as wages or self-employment income with FICA taxes paid, those years start building credits the same way any other job does. As of June 2026, no federal law grants Social Security credit for unpaid family care work, so the only path to earning those credits today is getting paid through an actual program. The difference between a record full of zeros and one with documented caregiver wages follows you for every month you collect a retirement benefit, for the rest of your life.

Here's something most family caregivers never find out until they pull their Social Security statement at 62: the years you spent caring for your mom, your dad, or your disabled spouse for free counted as zeros toward your retirement. The biggest gap in social security caregiver credits is that unpaid caregiving earns you none. Not partial credit. Zero. Your benefit is calculated on your 35 highest-earning years, and every year you didn't draw a reported income drags that average down.

That's the bad news, and it's worth understanding clearly before we get to the good news. Because once you start getting paid through a Medicaid program, the math changes in your favor. This guide walks through what Social Security credits actually are, why unpaid care leaves a hole in your record, and how getting paid to care for your loved one starts filling it back in.

Short version: unpaid caregiving builds no Social Security credits. Paid caregiving, reported correctly, does. The difference between those two situations can add up to real money in your retirement check decades from now.

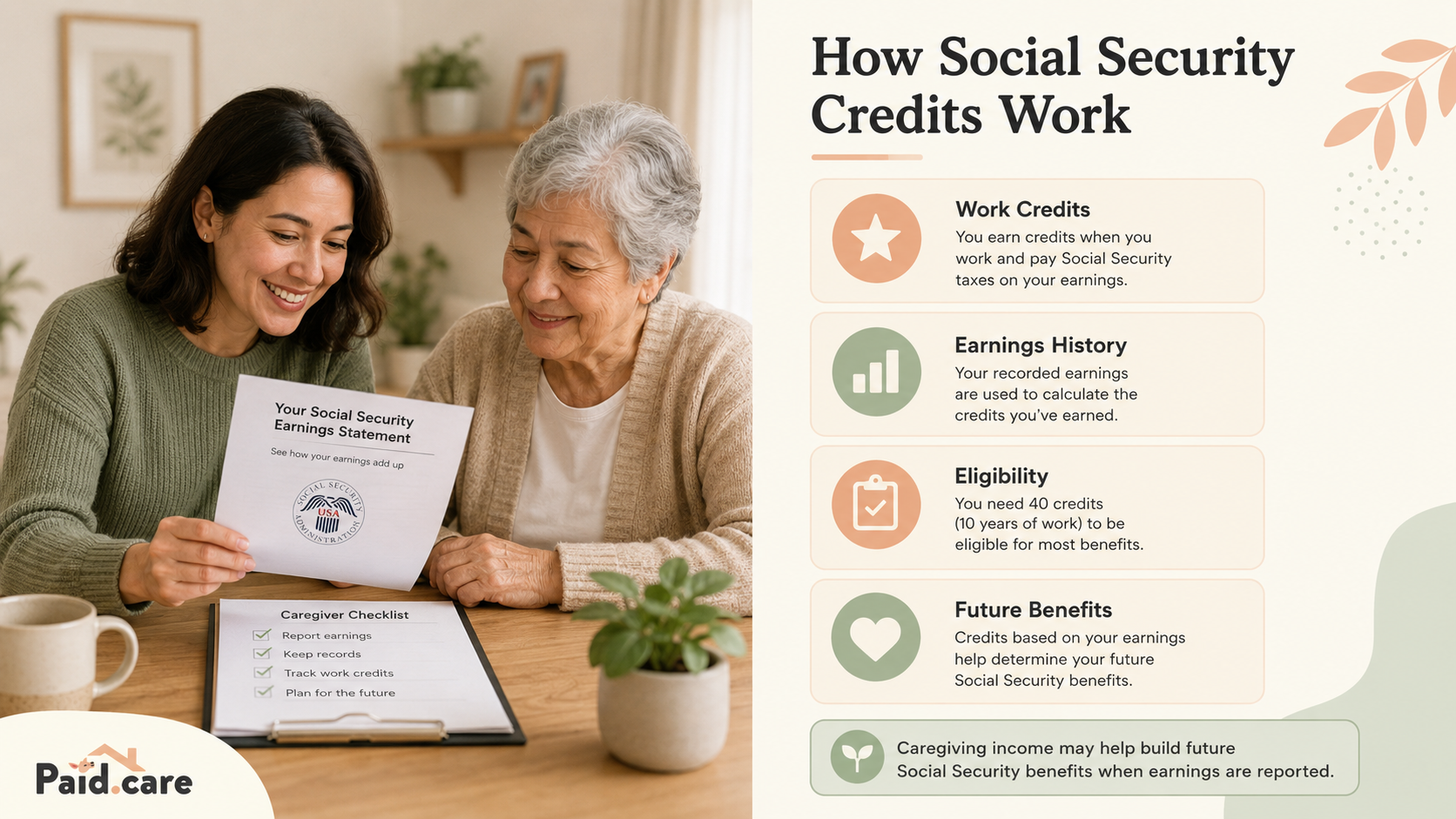

What Social Security credits actually are

Social Security runs on a credit system, not a years-worked system. You earn credits by working and paying Social Security taxes (the FICA line on your pay stub). In 2026, you get one credit for every $1,810 in covered earnings, and you can earn a maximum of four credits per year. So once you've earned roughly $7,240 in reported wages in a calendar year, you've maxed out your four credits for that year. Working more hours past that point doesn't add credits, though it does raise your earnings average.

You need 40 credits total to qualify for retirement benefits. That's ten years of work at four credits a year. Those credits also gate access to Social Security Disability Insurance (SSDI) if you become disabled, and they determine survivor benefits for your family. No credits, no benefit. It's that direct.

The catch for caregivers is that credits only come from reported, taxable earnings. Money has to flow through a payroll system or be reported as self-employment income for the Social Security Administration to see it. If you're caring for your father full time and the family is paying you in cash under the table, the SSA has no record that you worked at all. You're building nothing.

Why unpaid caregiving builds zero credits

Unpaid care is invisible to Social Security. The agency can't credit work it never sees on a tax return, and unpaid caregiving generates no W-2, no 1099, no FICA contribution. From the system's perspective, a caregiver who spends a decade caring for a parent at home looks identical to someone who didn't work at all for ten years.

The damage compounds in two ways. First, you're not earning the credits you need to qualify. Second, and this is the part people miss, those zero-earning years get folded into the 35-year average the SSA uses to calculate your monthly benefit. Say you worked 20 years before becoming a caregiver, then spent 10 years caring for a parent with no reported income. The SSA still uses 35 years in the formula. Those 10 caregiving years come in as zeros, and another 5 of your lowest early-career years fill out the rest. Your average earnings drop, and so does your check.

This is one of the quietest financial costs of family care, and it's covered in more depth in our look at the hidden costs of unpaid family care work in the US. The lost wages hurt now. The lost retirement credits hurt for the rest of your life.

A decade of unpaid caregiving doesn't just cost you a decade of income. It can lower your Social Security benefit for every month you collect it, for as long as you live.

How getting paid changes the math

When you're paid as a family caregiver through a Medicaid program and that income is reported correctly, you start earning Social Security credits again. This is the single biggest reason the shift from unpaid to paid caregiving matters for your long-term finances, far beyond the weekly check.

Most paid family caregiver arrangements run through one of two setups. In the W-2 employee model, you're an employee of an agency or a fiscal intermediary. They withhold FICA taxes, pay the employer share, and report your wages to the SSA. Those wages build credits automatically. In the self-employment or independent contractor model, you report the income yourself and pay self-employment tax, which also funds your Social Security record. The difference between these two affects your taxes and your benefits, and it's worth reading our breakdown of 1099 vs. W-2 for family caregivers before you assume which one you're in.

Here's a concrete picture. Imagine you start getting paid through a structured family caregiving program and report $18,000 in caregiver wages for the year. You've blown past the $7,240 threshold, so you earn the full four credits. You also add a real earnings year to your record instead of a zero. Do that for the years you'd otherwise have been caregiving unpaid, and you're protecting both your eligibility and your benefit calculation.

The mechanism is simple: reported income equals credits, credits equal eligibility, and consistent reported income raises your earnings average. Getting paid turns invisible work into a documented work history.

The one tax wrinkle every paid caregiver should know

There's a real complication here, and ignoring it can accidentally cost you credits. Under IRS Notice 2014-7, certain Medicaid waiver payments to a caregiver who lives in the same home as the care recipient can be excluded from federal income tax. That's often a good thing for your tax bill. But excluded income can, in some situations, mean no FICA contribution and therefore no Social Security credit for that money.

The interaction is genuinely tricky and depends on your exact arrangement, whether you're a household employee, and how the payments are reported. Some caregivers can elect to count the income for earned-income purposes even when it's excluded from taxable income. This is exactly the kind of decision where the tax-free benefit now can quietly trade against retirement credits later. Our guide on how a caregiver stipend differs from a caregiver wage at tax time walks through how the 2014-7 exclusion plays out, and you can read more on whether Medicaid waiver payments are taxable in your situation. Don't guess on this one. Confirm how your specific payment is being reported.

Credits, SSI, and SSDI are not the same thing

People mix these up constantly, and the distinction matters for caregivers because the answer to "will my pay hurt my benefits" depends entirely on which benefit you mean.

Social Security retirement and SSDI are earned through credits. More reported work means more credits and a higher eventual benefit. For these, getting paid as a caregiver helps you.

Supplemental Security Income (SSI) is a need-based program, not a credit-based one. It has strict income and asset limits. For SSI, caregiver income can actually reduce or eliminate your monthly payment if it pushes you over the limit.

So if you're a caregiver who receives SSI, you have to plan carefully. The same paycheck that builds your retirement credits could shrink your SSI check. If you're on SSDI, earning above the substantial gainful activity level can affect your benefit too. We cover this tension in detail in how caregiver pay affects disability benefits and SSI, and it's also worth understanding how caregiver income affects your own Medicaid eligibility since the two often move together. The right move depends on which benefits you're already receiving, so map that out before your first check arrives.

What about the old caregiver credit proposals?

You may have heard talk over the years about a federal "caregiver credit" that would give Social Security credit for years spent providing unpaid family care, similar to how some countries handle it. Bills along these lines have been introduced in Congress more than once. As of June 2026, no such credit for unpaid caregiving has become federal law. There is no automatic Social Security credit for unpaid family care work in the United States right now.

That's important because it means you can't count on a future fix to backfill the gap. The reliable way to earn social security caregiver credits today is to get paid through an actual program and have that income reported. Policy may change, and proposals keep coming back, but a credit that doesn't exist yet won't pay your future benefit. The paid route is the one that works now.

How paid caregiving in your state builds your record

If you live in Indiana, Michigan, or Illinois, there are working programs that pay family caregivers through Medicaid, and the income from these programs can count toward your Social Security record when it's reported as wages.

In Indiana, the Structured Family Caregiving program pays a daily stipend to caregivers living with their loved one. In Michigan, the Home Help program pays caregivers an hourly wage for personal care services. In Illinois, the Community Care Program compensates caregivers helping older adults stay at home. The way each program reports your income determines whether it builds Social Security credits, which loops back to that W-2 versus stipend question above.

The path from unpaid to paid is more direct than most families expect once they understand the steps. Our walkthrough on how to transition from unpaid to paid caregiver lays out the sequence, and if you're trying to picture the whole process, our How It Works page shows how qualification and payment fit together. Every week you're caring for free is a week you could be earning both a paycheck and a credit toward retirement.

What to do right now

Start by pulling your actual Social Security record. Create an account at the SSA and look at your earnings history. You'll see exactly which years show income and which show zeros. The caregiving years will likely be blank. That blank is what you're working to fix.

Then take these steps in order:

Find out which paid caregiver program your loved one qualifies for in your state, and how it reports caregiver income.

Confirm whether your payments will be reported as wages (W-2) or excluded under Notice 2014-7, and understand what each means for your credits.

Check how the income interacts with any SSI, SSDI, or Medicaid coverage you personally receive before you enroll.

Build the paid income into a long-term plan, since credits are only one piece of your financial picture.

That last step matters more than people think. The retirement credit gap is real, but so are taxes, benefit limits, and budgeting on caregiver pay. Our guide on financial planning for paid family caregivers and the broader look at financial benefits beyond the weekly paycheck tie these pieces together. Retirement planning is harder for caregivers, and our notes on retirement planning for the full-time caregiver go deeper on protecting your future self.

Frequently asked questions

Do I earn Social Security credits for unpaid family caregiving?

No. Unpaid caregiving builds zero social security caregiver credits because the work generates no reported, taxable income. Credits come only from earnings that pass through payroll or are reported as self-employment income. As of June 2026, there is no federal law that grants Social Security credit for unpaid family care work, despite proposals that keep surfacing in Congress.

If I get paid through Medicaid, will that count toward my Social Security?

It can, but only if the income is reported as wages or self-employment income with FICA or self-employment tax paid on it. When you're a W-2 employee of an agency or fiscal intermediary, your wages build credits automatically. If your payments are excluded from income under IRS Notice 2014-7, the situation gets more nuanced, and some of that money may not generate credits unless you handle the reporting carefully. Confirm with whoever processes your pay how your specific income is being reported.

How many credits do I need to qualify for Social Security?

You need 40 credits to qualify for retirement benefits, which equals about ten years of covered work. In 2026 you earn one credit per $1,810 in earnings, up to four credits per year, so you max out your annual credits at roughly $7,240 in reported income. Disability benefits through SSDI may require fewer credits depending on your age when you become disabled.

Can getting paid as a caregiver lower my SSI?

Yes, it can. SSI is need-based with strict income and asset limits, so caregiver pay can reduce or eliminate your SSI check even while it helps your retirement record. SSI and Social Security retirement work on opposite logic, which is why caregivers receiving SSI need to plan before enrolling in a paid program.

Will those caregiving zeros permanently lower my benefit?

The zeros count in your 35-year earnings average, so they do lower your calculated benefit. The fix is to add real earning years going forward. Years of reported caregiver income replace zeros in the formula, which raises your average and your monthly check over time.

The takeaway is direct: unpaid care earns you nothing toward retirement, and paid care reported correctly earns you both income and social security caregiver credits. If you're already doing the work, the smartest move is to get paid for it. See how the qualification and payment process works and find out which program in Indiana, Michigan, or Illinois can start building your record this year.