Caregiver Stipend vs. Caregiver Wage: What the Difference Means for Your Taxes

Family caregivers paid through stipends and those paid through wages face different federal tax obligations, and the distinction affects everything from quarterly estimated payments to self-employment tax. Stipends typically arrive without any withholding and generate a 1099, while wages come with taxes withheld at the source and generate a W-2. Under IRS Notice 2014-7, caregivers who live with their care recipient and receive payments through a Medicaid-funded waiver program can exclude those payments from federal gross income entirely, whether the payment arrives as a stipend or a wage. W-2 employees automatically build Social Security credits through payroll, while stipend-based caregivers who qualify for the tax exclusion and pay no self-employment tax do not accumulate those credits. Excludable Medicaid waiver income still counts as earned income for Earned Income Tax Credit purposes, so filing a federal return is the right move even when no tax is owed.

The words "stipend" and "wage" get tossed around interchangeably in family caregiver programs, but the IRS treats them very differently. Understanding the difference between a caregiver stipend and a caregiver wage for tax purposes can affect how much of your pay you actually keep, whether you owe self-employment tax, and how your income shows up when you apply for benefits like Medicaid or subsidized health insurance. Getting this wrong doesn't just cost you money at tax time. It can trigger penalties or jeopardize coverage your family depends on.

Here's what separates these two payment types, how each one flows through your tax return, and which questions to ask your program coordinator before you file.

What Counts as a Caregiver Stipend

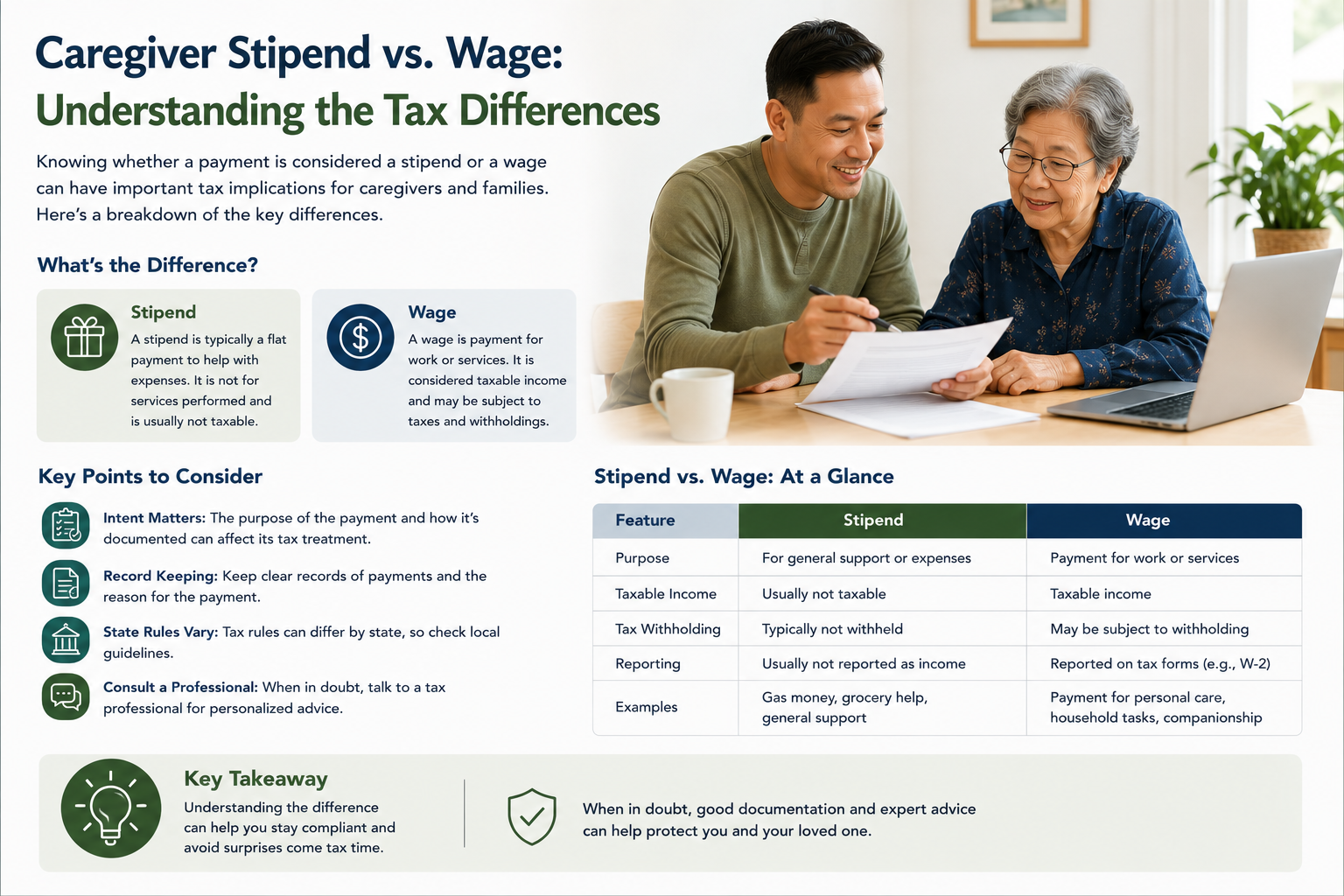

A stipend is a flat-rate payment meant to offset the costs of caregiving. It's typically not tied to a specific number of hours worked. Programs like Structured Family Caregiving in Indiana pay a daily rate — the caregiver receives a set dollar amount per day regardless of whether the care that day took four hours or fourteen. The VA's Program of Complete Assistance for Family Caregivers (PCAFC) works similarly, paying a monthly stipend pegged to the veteran's disability level rather than the caregiver's hours logged.

Stipends often arrive without taxes withheld. No one deducts federal income tax, Social Security, or Medicare from the payment before it hits your bank account. That full deposit can feel generous in January, but it creates an obligation you need to plan for. Because nothing is being taken out on the front end, the IRS expects you to account for that income yourself.

Tax Treatment of Stipends

Most caregiver stipends are considered taxable income. The IRS views them as compensation for services, even when the program labels the payment a "stipend" or "allowance." You'll typically receive a 1099-NEC or 1099-MISC at year's end, and you're responsible for reporting the full amount on your federal return.

There's one major exception. Under IRS Notice 2014-7, Medicaid waiver payments made to a caregiver who lives with the person receiving care can be excluded from gross income. If you live with your care recipient and get paid through a state Medicaid waiver program, your stipend may be tax-free at the federal level. This exclusion applies to programs in Indiana, Michigan, Illinois, and most other states. You can learn more about whether Medicaid waiver payments are taxable and how to claim the exclusion properly.

If the exclusion doesn't apply to you — say you don't live with your care recipient, or the payment comes from a non-Medicaid source — you'll owe federal income tax on the stipend. You may also owe self-employment tax (15.3% for Social Security and Medicare) if you're classified as an independent contractor. That's a significant bite.

What Counts as a Caregiver Wage

A wage is an hourly or salaried payment made to someone classified as an employee. The employer, often a home care agency, a fiscal intermediary, or in some states the care recipient themselves, withholds federal income tax, Social Security tax, and Medicare tax from each paycheck. You receive a W-2 at the end of the year instead of a 1099.

Programs that pay caregivers as W-2 employees include Michigan's Home Help Program and Illinois's Community Care Program, both of which route payments through agencies or fiscal intermediaries that handle payroll. If you're working through Michigan's Home Help system or enrolled in Illinois's Community Care Program, your pay is structured as a wage.

Tax Treatment of Wages

With a wage, the tax math is more familiar. Your employer withholds taxes throughout the year, so you're less likely to face a surprise bill in April. The employer also pays their share of Social Security and Medicare taxes on your behalf — that 7.65% employer match that independent contractors have to cover themselves.

Wages still count as taxable income on your federal return unless the IRS Notice 2014-7 exclusion applies. And it often does: if you live with your care recipient and the payment flows through a Medicaid waiver, the exclusion can zero out your taxable wages. In that case, your W-2 might show wages in Box 1 but the amount is excludable. Some fiscal intermediaries have started issuing W-2s that already reflect the exclusion (showing $0 in Box 1), though this varies by state and agency.

Even when the exclusion applies, the income still counts for earned income credit purposes. That's actually good news — it means you can potentially qualify for the Earned Income Tax Credit even though you don't owe income tax on the payments. If you're filing taxes for the first time as a paid caregiver, the 2026 guide to caregiver tax deductions and credits walks through what else you can claim.

Side-by-Side Comparison: Stipend vs. Wage

| Criteria | Caregiver Stipend | Caregiver Wage |

|---|---|---|

| Payment structure | Flat daily or monthly rate | Hourly or salaried, tied to hours worked |

| Tax withholding | None; you receive the full amount | Federal income tax, Social Security, and Medicare withheld |

| Tax form received | 1099-NEC or 1099-MISC | W-2 |

| Self-employment tax owed | Yes (15.3%) unless IRS 2014-7 exclusion applies | No; employer pays their half |

| IRS Notice 2014-7 exclusion eligible | Yes, if Medicaid-funded and living with care recipient | Yes, if Medicaid-funded and living with care recipient |

| Social Security credits earned | Only if self-employment tax is paid | Yes, automatically through payroll |

| Unemployment insurance eligibility | Typically no | Varies by state, but often yes |

The pattern here matters for long-term planning. If you're paid as a W-2 employee for years, you're building Social Security credits that count toward your retirement. Stipend-based caregivers who qualify for the tax exclusion and pay no self-employment tax aren't accumulating those credits. That's a tradeoff worth thinking about, especially if caregiving is your primary occupation for a long stretch. The retirement planning guide for full-time caregivers covers this in more detail.

How the IRS Notice 2014-7 Exclusion Changes Everything

This single IRS ruling is probably the most important piece of tax guidance for family caregivers, and it applies equally to stipends and wages. If you provide care under a Medicaid-funded waiver program and you live in the same home as your care recipient, the payments can be excluded from your federal gross income.

"Excluded from gross income" means exactly what it sounds like. You don't pay federal income tax on the money. If you're receiving a stipend classified as self-employment income, the exclusion also wipes out the self-employment tax obligation. For a caregiver receiving $30,000 a year in Medicaid waiver payments, that exclusion can save thousands.

But the exclusion has clear requirements. You must live with the person you're caring for. The program must be funded through Medicaid (not Medicare, not private pay, not a state-only program that doesn't use Medicaid dollars). And you need to report the income correctly on your return, even though it's excludable. Some caregivers skip filing altogether because they assume tax-free means no paperwork. Filing protects you from future questions and lets you claim credits you might be eligible for.

State income taxes are a separate question. Indiana, Michigan, and Illinois each have their own rules about whether they follow the federal exclusion. In practice, most states that fund their caregiver programs through Medicaid waivers do conform, but it's worth confirming with your state's tax authority or a tax preparer who understands caregiver income. The guide to reporting caregiver stipends on state taxes breaks this down state by state.

How Each Payment Type Affects Your Benefits

Taxes aren't the only place where the stipend-versus-wage distinction shows up. Your caregiver income, however it's classified, can affect your eligibility for Medicaid, SSI, SNAP, and marketplace health insurance subsidies.

If your payments qualify for the IRS 2014-7 exclusion, the income is excluded from your adjusted gross income (AGI). A lower AGI can keep you eligible for programs with income thresholds. But some benefit programs count gross income before tax exclusions, or they count income differently than the IRS does. SSI, for example, looks at "countable income" using its own formula, and caregiver payments may count even if they're federally tax-exempt.

For caregivers receiving wages through a W-2, the income reporting is automatic — it shows up in earnings databases that benefits agencies check. Stipend income reported on a 1099 can be harder for agencies to track, but that doesn't mean you can ignore it. Underreporting income to maintain benefits eligibility is fraud, and the consequences are serious. If you're worried about how your caregiver pay interacts with your own coverage, read through how caregiver income affects your Medicaid eligibility and whether caregiver pay will affect your disability benefits or SSI.

Which Payment Type Should You Expect?

You usually don't get to choose. The payment structure is determined by your state's program design and the agency or fiscal intermediary that manages your enrollment.

Structured Family Caregiving programs — like the one Paid.care runs in Indiana — typically pay daily stipends. Consumer-directed programs in Michigan and Illinois typically pay hourly wages through a fiscal intermediary. The VA's PCAFC pays monthly stipends. Private family arrangements (where a family member pays another family member directly) could be structured either way, though these carry additional tax complexities around household employer rules.

What you can do is ask the right questions before you start receiving payments:

Will I receive a W-2 or a 1099 at year-end?

Are taxes being withheld from my payments?

Does this program qualify under IRS Notice 2014-7?

If I live with my care recipient, will the fiscal intermediary adjust my W-2 to reflect the exclusion?

Do I need to make quarterly estimated tax payments?

Getting answers to these five questions before your first payment arrives saves you from scrambling in March. If you're still figuring out which program you qualify for, Paid.care's process page explains how to get matched with the right Medicaid caregiver program for your state and situation.

Common Mistakes to Avoid

The most frequent tax problem for family caregivers is doing nothing. You receive payments all year, no taxes are withheld, and then you face a tax bill plus penalties the following April. If you're receiving a stipend without withholding and the 2014-7 exclusion doesn't apply, you need to pay quarterly estimated taxes. The IRS expects payments in April, June, September, and January. Missing these deadlines triggers underpayment penalties regardless of your good intentions.

Another common mistake: assuming every Medicaid-funded payment qualifies for the 2014-7 exclusion. The exclusion specifically requires that you live with the care recipient. If your parent lives in their own home and you drive over daily to provide care, the exclusion likely doesn't apply — even though the program is funded through Medicaid. The "live-in" requirement is the gatekeeping factor.

A third issue comes up when caregivers receive both excludable and non-excludable income in the same year. Say you cared for your mother at home for eight months (excludable) and then she moved to a facility while you continued receiving some transition payments (potentially not excludable). You'd need to split the income on your return. A tax preparer familiar with the 1099 vs. W-2 distinction for family caregivers can help you sort this out.

Decision Matrix: Which Scenario Fits You?

Use this quick reference to figure out your likely tax situation based on your program type and living arrangement:

| Your situation | Payment type | Likely tax outcome |

|---|---|---|

| Medicaid waiver program, live with care recipient, paid as employee (W-2) | Wage | Federally tax-exempt under 2014-7; may still qualify for EITC |

| Medicaid waiver program, live with care recipient, paid as contractor (1099) | Stipend | Federally tax-exempt under 2014-7; no self-employment tax owed |

| Medicaid waiver program, do NOT live with care recipient, W-2 | Wage | Taxable income; taxes withheld automatically |

| Medicaid waiver program, do NOT live with care recipient, 1099 | Stipend | Taxable income plus self-employment tax; quarterly payments needed |

| VA PCAFC stipend | Stipend | Generally excluded from federal income under 38 U.S.C. § 1720G |

| Private family pay arrangement | Either | Fully taxable; household employer rules may apply |

If your situation doesn't fit neatly into one row, that's normal. Caregiver tax situations are often layered, especially when programs change mid-year or when multiple family members share caregiving duties. The guide to financial benefits beyond your weekly paycheck covers additional credits and exclusions that might apply to your filing.

Frequently Asked Questions

Is a caregiver stipend the same as a caregiver wage for tax purposes?

No. A caregiver stipend and a caregiver wage are taxed differently. Stipends typically arrive without any tax withholding and are reported on a 1099, which may require you to pay self-employment tax. Wages come with taxes already withheld and are reported on a W-2. Both can qualify for the IRS Notice 2014-7 exclusion if the payments are Medicaid-funded and you live with your care recipient, but the paperwork and quarterly tax obligations differ significantly.

Do I need to file taxes if my caregiver payments are excluded under IRS Notice 2014-7?

Yes, you should still file a federal tax return. Even though the income is excludable, filing protects you from future audits and allows you to claim valuable credits like the Earned Income Tax Credit. Your excludable income still counts as earned income for EITC purposes, which could put money back in your pocket.

How do I know if my state follows the federal tax exclusion for caregiver payments?

Most states with Medicaid-funded caregiver programs do follow the federal exclusion, but there are exceptions. Check with your state's department of revenue or consult a tax preparer experienced with caregiver income. For Indiana, Michigan, and Illinois specifically, the state-by-state reporting guide has current details.

What happens if I don't make quarterly estimated tax payments on my caregiver stipend?

The IRS charges an underpayment penalty, calculated on the amount you should have paid each quarter. The penalty isn't catastrophic. It functions like interest, but it adds up over four missed quarters. If you owe more than $1,000 at filing time and didn't make estimated payments, the penalty kicks in automatically.

Can I switch from receiving a stipend to receiving a wage?

That depends on your state's program structure and the agency managing your care plan. Some states offer both consumer-directed options (where you're paid as an employee of the care recipient) and structured programs (where you receive a daily stipend). If you want to change how your income is classified, talk to your program coordinator or reach out to Paid.care to see what options exist in your state.