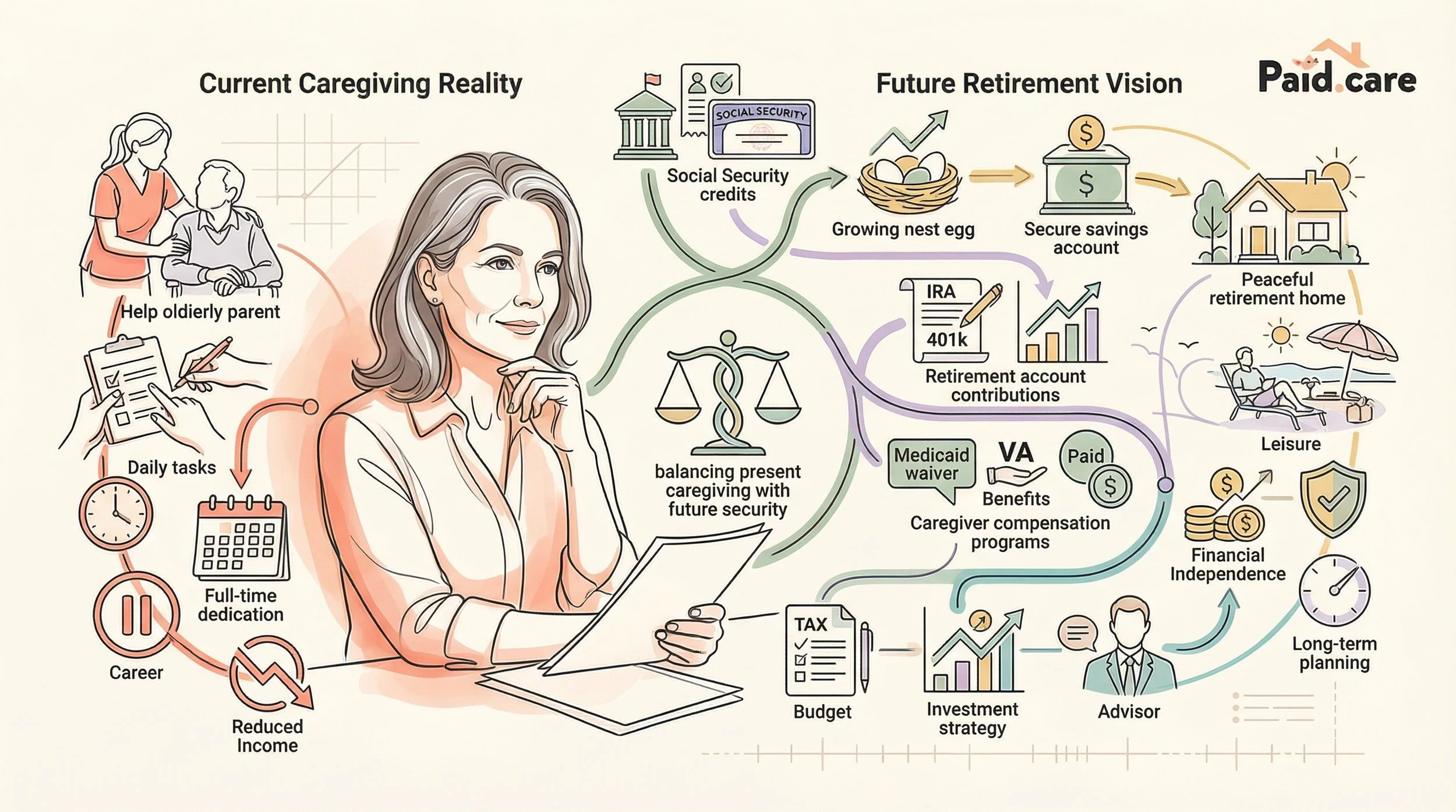

Retirement Planning for the Full-Time Caregiver: Essential Financial Strategies and Benefits

Full-time caregivers play a crucial role in supporting their loved ones, yet they often overlook their own financial futures. Retirement planning for caregivers is essential, as it ensures they can maintain their quality of life after years of dedicated service. This article will explore effective strategies for caregivers to save for retirement, the benefits available through Medicaid and Medicaid waivers, tax incentives, and long-term care planning options. By understanding these financial strategies, caregivers can secure their financial well-being while continuing to provide care.

How Can Full-Time Caregivers Save Effectively for Retirement?

Saving for retirement can be particularly challenging for full-time caregivers due to the demands of their roles. However, understanding effective saving strategies can empower caregivers to build a secure financial future. Caregivers should prioritize retirement savings by exploring various "financial planning options" tailored to their unique needs.

What Are the Best Financial Planning Options for Caregivers?

Caregivers have several financial planning options available to them, including:

Individual Retirement Accounts (IRAs): These accounts allow caregivers to save for retirement with tax advantages. Traditional IRAs offer tax-deductible contributions, while Roth IRAs provide tax-free withdrawals in retirement.

Employer-Sponsored Retirement Plans: If caregivers are employed, they may have access to 401(k) plans, which often include employer matching contributions, enhancing their savings potential.

Health Savings Accounts (HSAs): For caregivers with high-deductible health plans, HSAs offer a way to save for medical expenses while also providing tax benefits.

By utilizing these financial planning options, caregivers can effectively save for their retirement while managing their caregiving responsibilities.

How Do Retirement Savings Plans Adapt to Caregiver Needs?

Retirement savings plans can be tailored to meet the specific needs of caregivers. Many plans now offer flexible contribution options, allowing caregivers to adjust their savings based on their financial situation. Additionally, some plans provide resources and support specifically designed for caregivers, such as financial counseling and educational materials. This adaptability is crucial for caregivers who may face fluctuating income levels or unexpected expenses related to their caregiving duties.

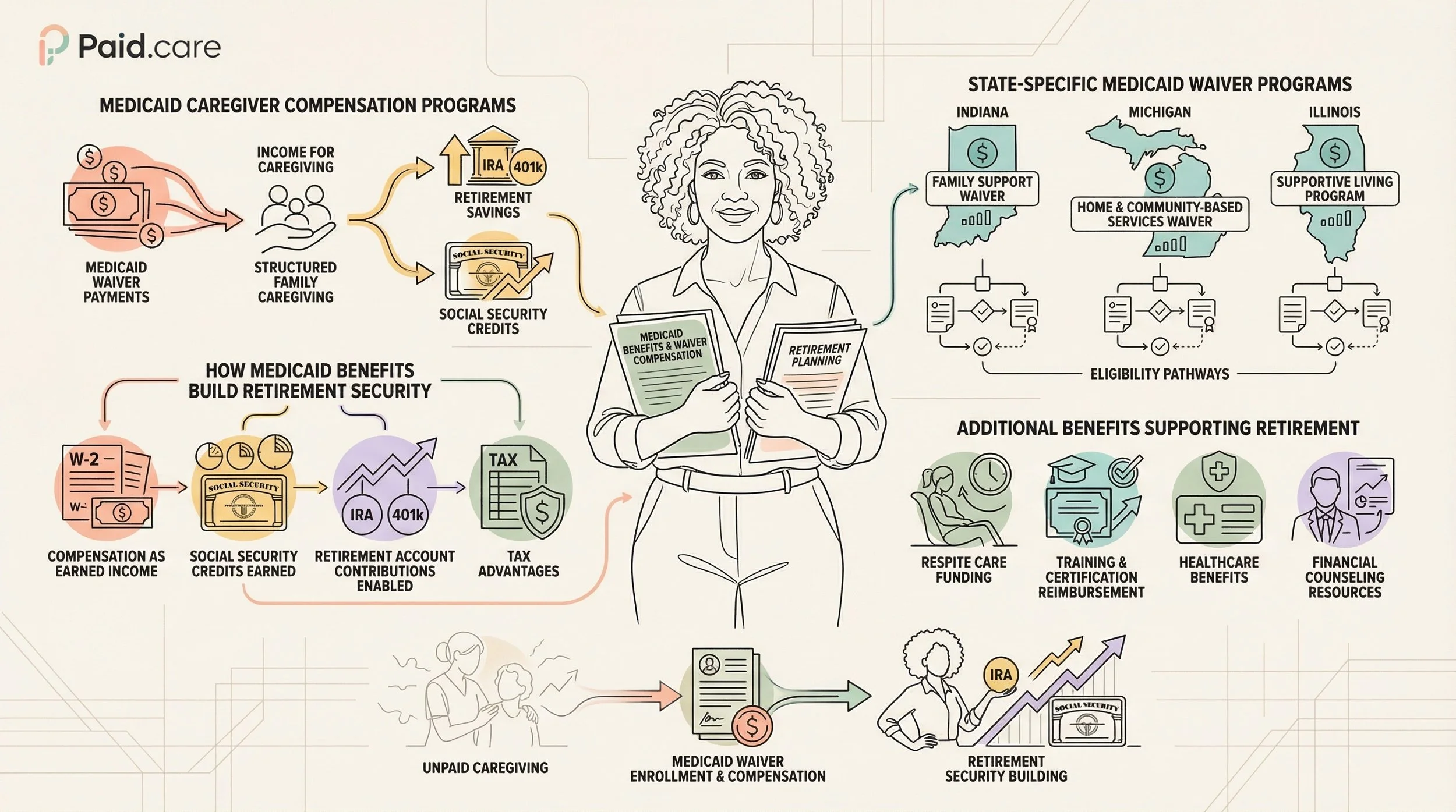

What Medicaid and Medicaid Waiver Benefits Support Caregiver Retirement?

Medicaid and Medicaid waiver programs can provide essential financial support for caregivers, helping them secure their retirement. These programs offer various benefits that can alleviate the financial burden of caregiving, allowing caregivers to focus on their own financial futures.

What Are the Eligibility Criteria for Caregivers to Access Medicaid Benefits?

To access Medicaid benefits, caregivers must meet specific eligibility criteria, which typically include:

Income Limits: Caregivers must have an income below a certain threshold, which varies by state.

Asset Limits: There are also limits on the amount of assets caregivers can own while still qualifying for benefits.

Functional Needs: Caregivers must demonstrate a need for assistance with daily living activities, which can be assessed through a state evaluation process.

By understanding these criteria, caregivers can better prepare for the application process and secure the benefits that support their retirement planning.

Which Tax Benefits and Credits Are Available for Family Caregivers?

Family caregivers may be eligible for various tax benefits and credits that can significantly impact their financial situation. These incentives can help reduce the overall tax burden, allowing caregivers to allocate more resources toward their retirement savings.

How Can Caregivers Maximize Tax Deductions and Credits?

Caregivers can maximize their tax benefits by:

Claiming the Dependent Care Credit: This credit allows caregivers to claim expenses incurred while caring for a dependent, reducing their taxable income.

Utilizing Medical Expense Deductions: Caregivers can deduct unreimbursed medical expenses for their dependents, which can include costs related to caregiving.

Taking Advantage of the Earned Income Tax Credit (EITC): This credit is available to low- to moderate-income workers, providing a significant tax break that can enhance savings.

By leveraging these tax benefits, caregivers can improve their financial standing and contribute more effectively to their retirement plans.

What Are the State-Specific Tax Incentives for Caregivers in the Midwest?

In addition to federal tax benefits, several states in the Midwest offer specific tax incentives for caregivers. For example:

Indiana: Offers a caregiver tax credit for those providing care to eligible individuals.

Michigan: Provides a tax deduction for certain caregiving expenses.

Illinois: Has a tax credit for family caregivers who incur out-of-pocket expenses for care.

These state-specific incentives can further enhance the financial resources available to caregivers, supporting their retirement planning efforts.

What Long-Term Care and Legal Planning Options Should Caregivers Consider?

Long-term care and legal planning are critical components of retirement planning for caregivers. By addressing these areas, caregivers can ensure they are prepared for future needs and protect their financial interests.

How Does Long-Term Care Insurance Support Retirement for Caregivers?

Long-term care insurance can provide financial support for caregivers by covering the costs associated with extended care services. This type of insurance can help alleviate the financial burden of caregiving, allowing caregivers to focus on their own retirement savings. Policies typically cover services such as in-home care, assisted living, and nursing home care, providing peace of mind for caregivers as they plan for their future.

What Estate and Legal Planning Steps Are Essential for Family Caregivers?

Family caregivers should consider several essential estate and legal planning steps, including:

Creating a Will: A will ensures that a caregiver's assets are distributed according to their wishes after their passing.

Establishing Power of Attorney: This legal document allows caregivers to designate someone to make financial or medical decisions on their behalf if they become unable to do so.

Reviewing Beneficiary Designations: Caregivers should regularly review and update beneficiary designations on retirement accounts and insurance policies to reflect their current wishes.

By taking these steps, caregivers can protect their assets and ensure their financial security as they transition into retirement.

FAQs

-

If you are married and filing jointly, you can utilize a Spousal IRA. This allows you to contribute to a Traditional or Roth IRA based on your spouse’s income, even if you do not have a paycheck of your own. For 2026, the standard contribution limit is $7,500. If you are age 50 or older, you can add a "catch-up" contribution of $1,100 (totaling $8,600), and those aged 60–63 can take advantage of the new "super catch-up" rules for employer-sponsored plans to boost savings even further.

-

Yes, but in a positive way. If you participate in the "Paycheck Pivot"—transitioning to a paid caregiver role via state-funded programs like CDPAP or IHSS—your earnings are typically subject to FICA taxes. This means you continue to earn Social Security "work credits" toward your own future retirement benefits. In 2026, you earn one credit for every $1,890 in wages, up to a maximum of four credits per year. This prevents "zero-earning years" from lowering your future monthly Social Security checks.

-

While not a direct retirement "match," tax credits free up the cash flow needed to invest. You should claim the "Credit for Other Dependents," which provides up to $500 for a qualifying adult relative. Additionally, the "Child and Dependent Care Credit" allows you to claim up to $3,000 in expenses ($6,000 for two or more) if you pay for respite care or adult day care so you can work. In 2026, the Dependent Care FSA limit has also increased to $7,500, allowing you to use pre-tax dollars for caregiving expenses, which reduces your taxable income.

-

As of 2026, a federal "Social Security Caregiver Credit"—which would provide retirement credits for unpaid caregiving—has been proposed in Congress but is not yet law. To protect your retirement in the meantime, you must rely on "Spousal Benefits" (where you can claim up to 50% of a spouse’s benefit) or ensure you are receiving a formal wage through state self-directed care programs. Documenting your caregiving hours is essential for qualifying for these paid programs and ensuring you don't face a "retirement gap" later in life.