Why the Caregiver Tax Credit Falls Short for Most Families and What Actually Helps

The caregiver tax credit gets talked about like it's a paycheck for family caregivers. It isn't. A federal tax credit only matters at tax time, only helps if you owe taxes, and almost never matches what you've actually spent caring for an aging parent or a disabled spouse. If you've been waiting on a caregiver tax credit to make the math work, you're waiting on the wrong thing.

Here's the short version: there is no single, fully refundable federal caregiver tax credit on the books that puts real money in most caregivers' pockets the way Medicaid payment programs do. What exists are scattered credits and deductions with tight rules, and a lot of proposed legislation that never crossed the finish line. The fix for most families in Indiana, Michigan, and Illinois isn't a deduction in April. It's getting paid weekly through a Medicaid program right now.

What the caregiver tax credit actually is (and isn't)

When people say "caregiver tax credit," they usually mean one of three things, and none of them work the way the name suggests.

The first is the Credit for Other Dependents, worth up to $500 if you claim a qualifying relative as a dependent. That's it. Five hundred dollars, once a year, and only if your parent or relative meets the IRS gross income test, which is low enough that most people receiving Social Security can blow past it. The second is the Child and Dependent Care Credit, which covers care expenses that let you work, but it's built around childcare and adult day care receipts, not the unpaid hours you put in yourself. The third is the medical expense deduction, where you can write off qualifying medical costs above 7.5% of your adjusted gross income, but only if you itemize, and only the portion above that floor.

Notice what every one of these has in common. They reward money you spent on someone else's care. None of them pay you for the care you provide with your own hands. A credit lowers a tax bill. It does not replace lost wages, cover the gas you burned driving to specialist appointments, or make up for the job you cut back to part-time. For a deeper breakdown of which write-offs genuinely apply, the rundown of tax deductions and credits family caregivers can claim in 2026 is worth a careful read before you file.

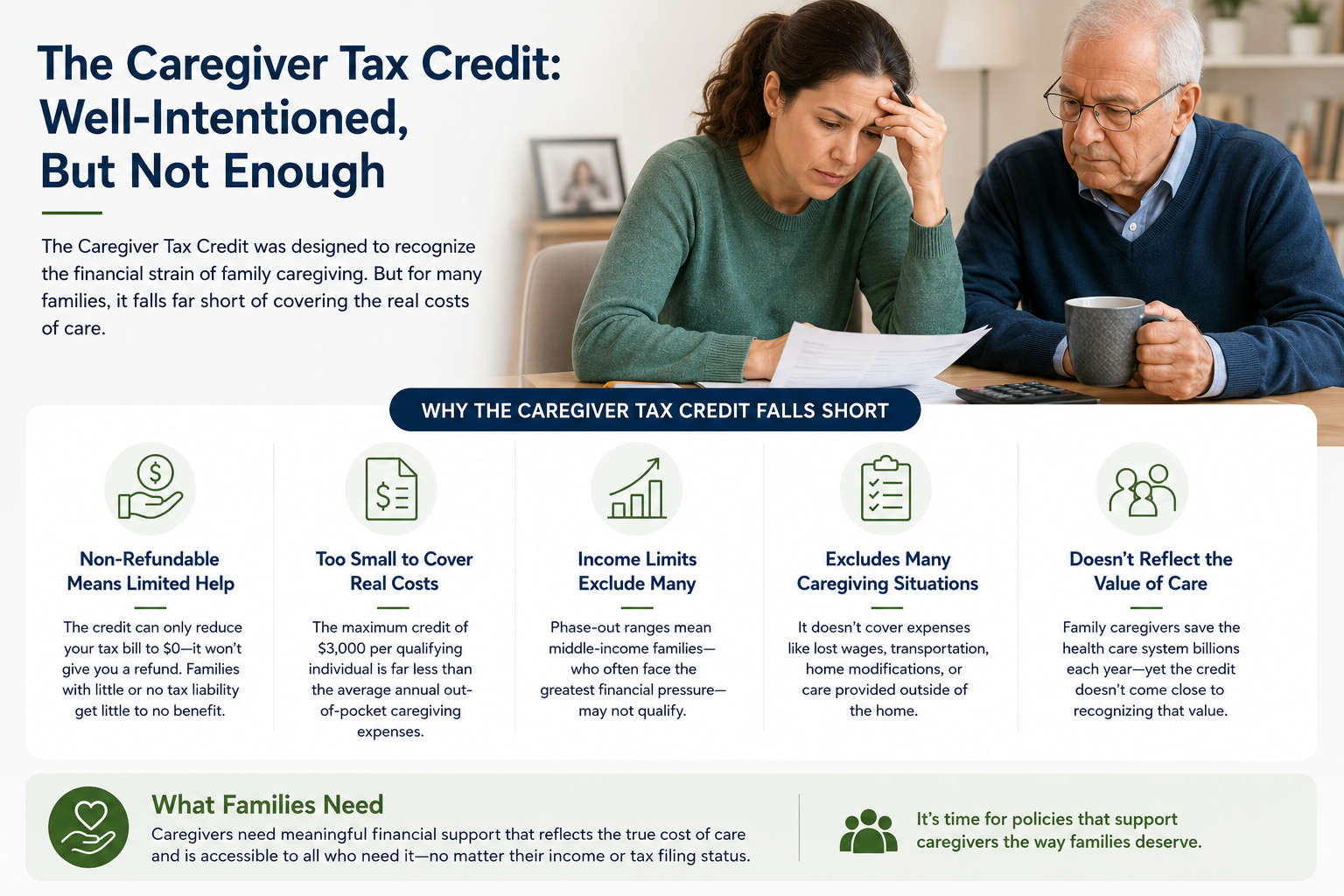

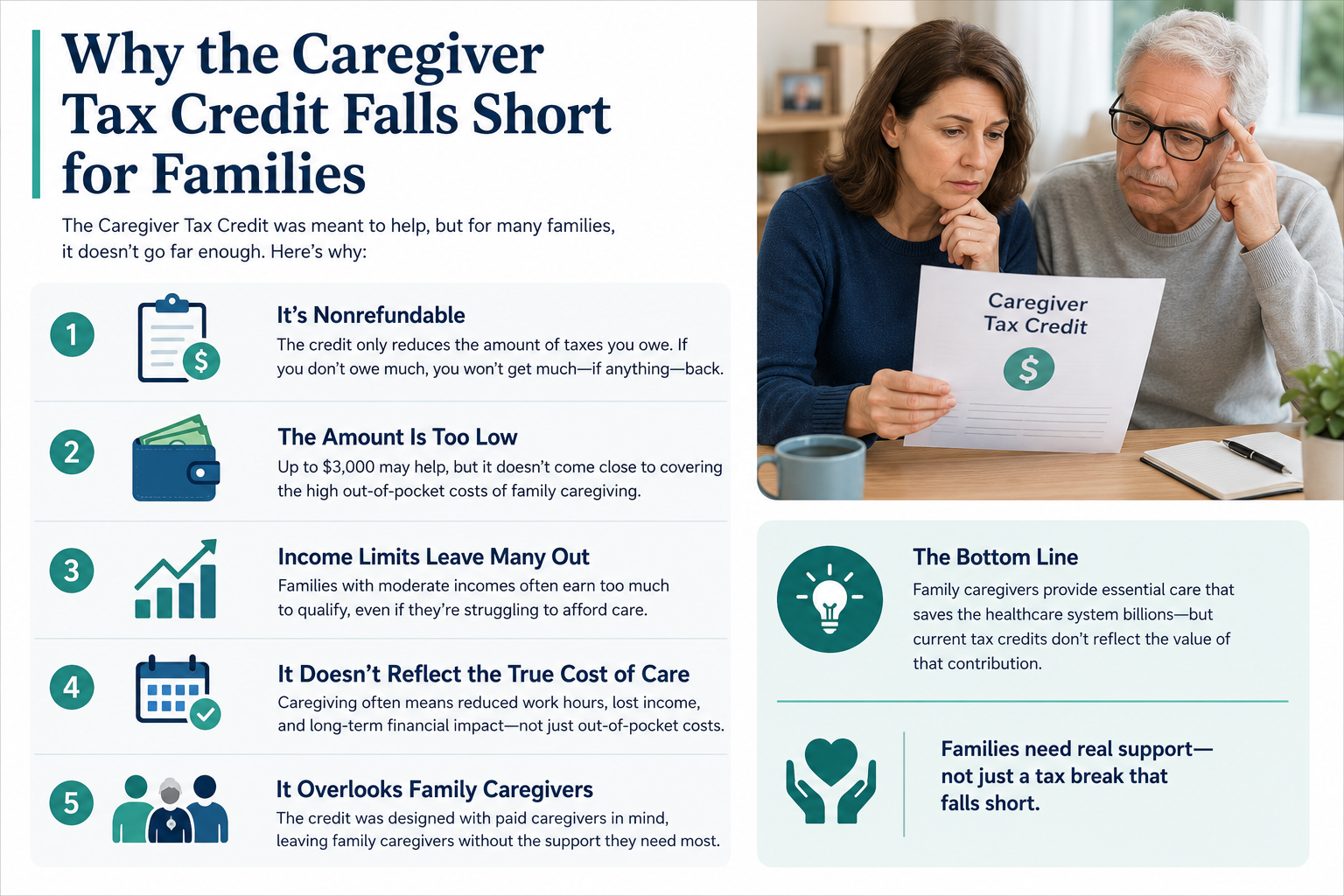

Why the credit falls short for most families

The gap between what caregiving costs and what a tax credit returns is enormous, and it comes down to a few hard limits baked into how credits work.

It's once a year, not weekly. Care costs hit every single week. Rent, groceries, copays, and your own bills don't wait for a refund. A credit that arrives months after you've already gone into debt isn't relief, it's reimbursement, and a partial one at best.

Most credits are nonrefundable. If you don't owe enough tax, a nonrefundable credit can only zero out your bill, not pay you the difference. Many caregivers, especially those who left work to provide care, have low taxable income to begin with. The credit they qualify for on paper shrinks to nothing in practice.

The dependent rules disqualify a lot of relatives. To claim your parent as a dependent, their gross income generally has to stay under the IRS threshold and you have to cover more than half their support. A parent on a modest pension or Social Security can fail that test, even though you're doing all the hands-on work.

It ignores the real cost: your time. The biggest expense in family caregiving is the income you give up. No tax credit on the books today values an hour of your labor. Medicaid caregiver programs do exactly that.

That last point is the whole game. The credit treats you like a generous payer of someone else's expenses. A paid caregiver program treats you like a worker who deserves a wage. Those are completely different financial outcomes.

The legislation everyone keeps hearing about

Every couple of years a bill floats through Congress promising a real, refundable credit for unpaid family caregivers, often in the range of a few thousand dollars a year. Versions of the Credit for Caring Act have been introduced repeatedly. As of June 2026, no broad federal refundable caregiver tax credit has become law. Promises in a press release don't show up on your return.

A handful of states have moved on their own, with limited caregiver credits tied to specific spending and income caps. If you want to see where state-level efforts and earlier proposals stood, the breakdown of how 2025 policy changes could expand caregiver tax credits walks through what was actually on the table versus what got signed. The honest read: planning your family's finances around a credit that might pass is a bad bet. Planning around a program you can enroll in this month is a good one.

What actually helps: getting paid for the care you already give

The strongest financial move for most unpaid caregivers isn't a credit. It's enrolling in a Medicaid program that pays you a wage for the care you're already providing. These run through Home and Community-Based Services waivers and consumer-directed care, and they exist specifically so families can keep loved ones at home instead of in a facility. Indiana, Michigan, and Illinois all have working versions right now.

In Indiana, that usually means Structured Family Caregiving or the Attendant Care program, where a family member living with and caring for an eligible adult receives a daily stipend or hourly pay. Michigan runs the Home Help program, which pays approved caregivers, including many relatives, an hourly rate for personal care. Illinois families can get paid through the Community Care Program and the IDHS Home Services Program. These aren't reimbursements at tax time. They're regular checks for hours worked.

Here's the difference laid out plainly:

| Feature | Caregiver tax credit | Medicaid caregiver payment |

|---|---|---|

| When you get money | Once a year, after filing | Weekly or biweekly |

| What it pays for | Expenses you spent on someone else | The care work you personally do |

| Income requirement to benefit | Must owe tax (most are nonrefundable) | Pays regardless of your tax bill |

| Typical value | Up to a few hundred dollars | Hundreds to thousands per month |

| Available now | Limited, narrow eligibility | Yes, through state waivers |

There's a tax angle here too, and it works in your favor. Under IRS Notice 2014-7, certain Medicaid waiver payments to a caregiver living in the same home as the care recipient can be excluded from gross income. That means in some situations, the money you earn as a paid family caregiver isn't taxed the way ordinary wages are. The mechanics matter and they're easy to get wrong, so the guide on the difference between a caregiver stipend and a caregiver wage at tax time is the one to bookmark before you file.

Protecting the benefits you already have

One real worry stops families from applying: will getting paid hurt the loved one's Medicaid or my own benefits? Usually no, but it depends on the program and your situation, and you want to get this right before the first check.

If you receive SSI or SSDI yourself, caregiver income can interact with your benefits, though most caregivers keep their coverage with the right setup. The specifics on whether caregiver pay affects disability benefits or SSI are worth reviewing if that's your case. And if you're on Medicaid for your own health coverage, understand how the new income is counted, because there are ways to protect your Medicaid eligibility while earning caregiver income. None of these are dealbreakers. They're just steps, and skipping them is what creates problems, not the income itself.

The smarter financial plan

Treat the tax credit as a small add-on, not a strategy. Claim what you legitimately qualify for at tax time, keep your receipts for qualifying medical expenses, and check whether your state offers a caregiver-specific credit. Then build your actual plan around a steady paid caregiver program, because that's the income that shows up every week and covers real bills.

A tax credit gives you a few hundred dollars in spring. A Medicaid caregiver program can pay you every week of the year for work you're already doing for free.

Once you have paid caregiver income coming in, the next move is making it last. Setting aside for taxes if your payments are taxable, building a small cushion, and protecting any benefits in play turns a paycheck into stability. The walkthrough on building financial stability while getting paid to care covers how to do that from your first check forward.

Where to start

If you're in Indiana, Michigan, or Illinois and you've been counting on a caregiver tax credit to ease the financial squeeze, shift your energy toward enrollment in a paid program instead. The qualification process is simpler than most families expect, and you don't have to figure out the waivers, paperwork, and pay rates alone. Walk through how getting paid as a family caregiver works to see the steps, then look at the family caregiver pay rate guide to understand what your hours could actually be worth. A tax credit is a footnote. Getting paid is the real answer.

Frequently asked questions

Is there a federal caregiver tax credit I can claim right now?

Not a dedicated, refundable one that pays family caregivers for their time. As of June 2026, the caregiver tax credit most people qualify for is the Credit for Other Dependents (up to $500), and only if your relative meets the IRS dependent rules. You may also use the medical expense deduction or the Child and Dependent Care Credit, but each has narrow conditions and none replace lost income. Getting paid through a Medicaid caregiver program is the route that delivers real, regular money.

Can I get a tax credit and Medicaid caregiver pay at the same time?

In many cases, yes, though they serve different purposes. The tax credit relates to expenses and dependent status on your return, while Medicaid pay is a wage for care work. Some Medicaid waiver payments may even be excluded from your taxable income under IRS Notice 2014-7 when you live with the care recipient. Because the interaction depends on your exact situation, confirm the details with the program and a tax professional before filing.

Why is a Medicaid caregiver payment better than waiting on the credit?

It pays you for the hours you actually work, it arrives weekly or biweekly instead of once a year, and it doesn't require you to owe taxes to benefit. A caregiver tax credit can return a few hundred dollars; a paid program can pay hundreds or thousands a month depending on care needs and approved hours. For families covering real expenses every week, regular income beats an annual reimbursement.

Will getting paid as a caregiver cost my loved one their Medicaid?

Generally no. These payment programs run through Medicaid itself and are designed to keep your loved one at home rather than in a facility. Your own benefits, like SSI or SSDI, need a closer look, but most caregivers keep their coverage with the right planning. The key is understanding how the income is counted before you enroll.