How Caregiver Income Affects Medicaid Eligibility for the Caregiver Themselves

Caregiver pay from a Medicaid waiver program counts as income on your tax return, and that income is what Medicaid uses to determine your own eligibility. IRS Notice 2014-7 allows caregivers who live with the person receiving care to exclude those payments from gross income entirely, which keeps the money off your MAGI and protects your coverage. Whether your state respects that federal exclusion depends on how its Medicaid eligibility system is built, and Indiana, Michigan, and Illinois each handle it differently. Caregivers who lose coverage after starting a paid program most often lose it because they never claimed the exclusion, failed to report income changes on time, or counted household income incorrectly. Claiming the exclusion correctly, coordinating with a tax preparer who knows these rules, and contacting your state Medicaid office before your first paycheck arrives are the steps that keep your coverage intact while you get paid.

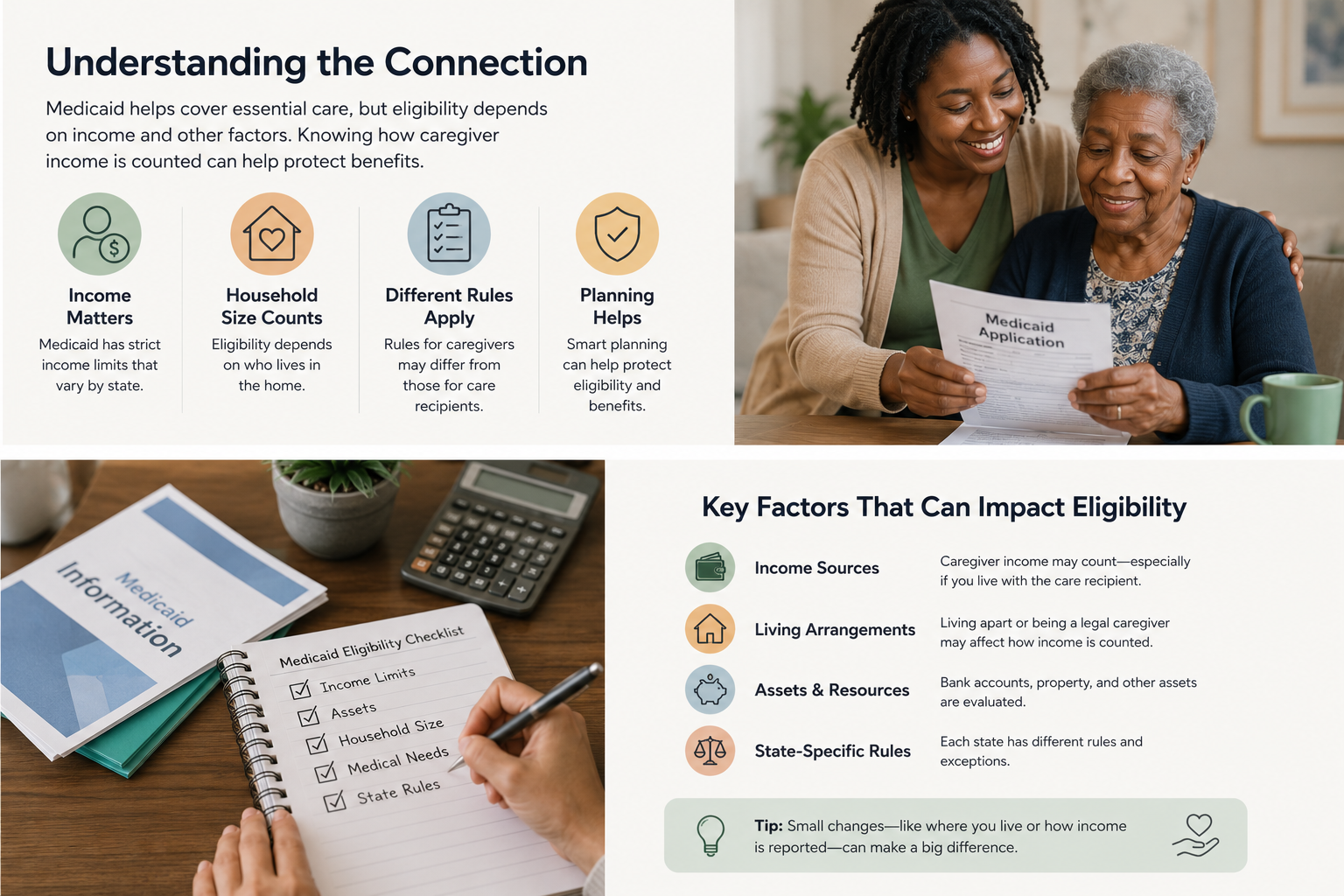

Earning money as a paid family caregiver through Medicaid can put your own Medicaid coverage at risk if you don't understand how the income gets counted. The fear is real: you finally start getting paid for the care you've been providing for free, and then a letter arrives saying your health insurance is under review. Understanding how caregiver income affects Medicaid eligibility for the caregiver themselves is the difference between building financial stability and accidentally losing the coverage your family depends on.

Most family caregivers who run into trouble here are simply caught off guard by how Medicaid counts different types of income, and by how the rules shift depending on which state you live in and which program pays you. This article breaks down why this problem happens and what you can do about it.

Why Caregiver Pay Can Trigger a Medicaid Problem

Medicaid eligibility is tied to your Modified Adjusted Gross Income, or MAGI. When you're an unpaid caregiver, your income is whatever else you earn (or don't earn). The moment you become a paid caregiver through a Medicaid waiver program, that payment shows up as income on your tax return, and Medicaid's eligibility system takes notice.

Here's where it gets tricky. Medicaid waiver payments can sometimes be excluded from gross income under IRS Notice 2014-7, which allows certain difficulty-of-care payments to be treated as tax-free. But "tax-free for federal income tax purposes" and "excluded from Medicaid income calculations" aren't always the same thing. Some states follow the federal exclusion when calculating Medicaid eligibility. Others count the gross payment regardless. And a few have their own carve-outs that land somewhere in between.

So two caregivers earning the exact same weekly amount through similar programs can have completely different Medicaid outcomes depending on their state. If you're providing care in Indiana, Michigan, or Illinois, the details matter even more because each state runs its caregiver payment programs differently.

How Different Caregiver Payment Types Get Counted

Not all caregiver pay is structured the same way, and the structure determines how Medicaid sees it.

W-2 Wages Through a Home Care Agency

If you're employed as a W-2 caregiver through an agency like the ones that administer Michigan's Home Help program or Illinois's Community Care Program, your pay is reported as wage income. It shows up on your W-2 and counts toward your MAGI. This is the most common arrangement, and it's the one most likely to push your income above Medicaid thresholds if you're not planning for it.

Stipends and Daily Rates

Programs like Structured Family Caregiving in Indiana often pay a daily stipend rather than an hourly wage. These stipends may qualify for the IRS Notice 2014-7 exclusion if the caregiver lives with the care recipient. When the exclusion applies, the income doesn't appear on your federal tax return at all, which typically means Medicaid won't count it either. But you need to confirm this with your state's Medicaid office, because the application of this rule varies.

Self-Directed or Consumer-Directed Pay

In consumer-directed programs, your loved one (or their representative) acts as the employer. How income gets reported depends on the fiscal intermediary handling payroll. Some intermediaries report the pay as wages; others issue it in a way that allows the difficulty-of-care exclusion. Ask the fiscal intermediary directly how they'll report your earnings to the IRS. That single answer shapes everything downstream.

The IRS Notice 2014-7 Exclusion, Explained Simply

IRS Notice 2014-7, issued in 2014, said that Medicaid waiver payments made to a caregiver who lives with the person receiving care can be excluded from gross income. The IRS treats these as "difficulty of care" payments, a category originally designed for foster care providers.

For federal taxes, this is clear. If you live with your care recipient and you're paid through a Medicaid waiver program, you can exclude that income from your federal return. You don't owe federal income tax on it.

For Medicaid eligibility, though, the question becomes: does your state's Medicaid program use your federal MAGI (which wouldn't include the excluded income) or does it look at your gross earnings before the exclusion? Most states that expanded Medicaid under the Affordable Care Act use MAGI-based calculations, which typically respect the federal exclusion. But states with legacy eligibility systems, or states that layer their own income rules on top, might not. If you want to understand how to report caregiver income without losing health coverage, the 2014-7 exclusion is the first thing to get right.

State-by-State Differences: Indiana, Michigan, and Illinois

Each of these three states handles caregiver income differently within its Medicaid system.

Indiana

Indiana uses MAGI-based Medicaid eligibility for most adults through the Healthy Indiana Plan (HIP). If your caregiver pay qualifies for the IRS 2014-7 exclusion and you properly exclude it from your federal return, Indiana's MAGI calculation should reflect that lower number. Caregivers in the Indiana Medicaid waiver programs who live with their care recipient are generally in the best position to claim this exclusion. That said, if you're earning additional income from another job, the combined total still matters. Indiana's Medicaid income limits apply to your total countable income, not just caregiver pay.

Michigan

Michigan's Home Help program pays caregivers as W-2 employees through agencies. Whether the 2014-7 exclusion applies depends on your living arrangement and the agency's reporting practices. Some agencies in Michigan have been inconsistent about whether they report these payments as excludable. You may need to work with a tax preparer who understands caregiver pay to file your return correctly, and then follow up with the Michigan Department of Health and Human Services if your Medicaid eligibility gets flagged. Check Michigan's current Medicaid income limits to see where you stand before and after the exclusion.

Illinois

Illinois runs its paid caregiver programs primarily through the Community Care Program. Caregivers here are typically employed through a home care agency and receive W-2 wages. The 2014-7 exclusion can apply if the living arrangement qualifies, but Illinois has its own wrinkles. The state expanded Medicaid broadly, so income limits are relatively generous for adults. Still, if you're a caregiver earning $15-$20 per hour for 30+ hours a week, that annual income can approach or exceed thresholds quickly, especially if a spouse's income is also in the picture. The Illinois caregiver application process doesn't always flag this issue upfront, so you need to track it yourself.

What to Do If Your Income Is Close to the Limit

If your caregiver income (after any applicable exclusions) puts you near your state's Medicaid income threshold, you have several real options. None of them require you to earn less.

Confirm your living arrangement qualifies for the 2014-7 exclusion. "Living with" the care recipient is the key requirement. If you do, make sure your employer or fiscal intermediary is reporting the payments correctly. Many caregivers lose out on this exclusion simply because no one told them to claim it.

Contribute to a pre-tax retirement account. Traditional IRA contributions reduce your MAGI. If you're a W-2 caregiver, your employer may offer a retirement plan. Even small monthly contributions can drop your countable income below the line. Retirement planning as a full-time caregiver isn't just a long-term play; it can protect your Medicaid eligibility right now.

Check whether your state offers a Medicaid "income disregard" for caregivers. Some states exclude a portion of earned income when determining eligibility, separate from the 2014-7 issue. These disregards vary widely and change periodically.

Look into Marketplace coverage as a backup. If your income rises above Medicaid limits, you may qualify for subsidized coverage through the ACA Marketplace. The transition isn't ideal, but it's not catastrophic either, especially if your caregiver pay is stable enough to budget for a low-premium plan.

The worst move is to avoid becoming a paid caregiver out of fear. Earning nothing protects your Medicaid eligibility, sure, but it also means you're doing a full-time job for free while your own financial security erodes. The smarter approach is to budget your caregiver pay intentionally and plan around the income thresholds directly.

Common Mistakes That Cause Caregivers to Lose Coverage

A few patterns come up repeatedly when caregivers lose their own Medicaid coverage after starting a paid program.

First, failing to update their Medicaid case when income changes. Medicaid requires you to report income changes, usually within 10 to 30 days depending on your state. If you go from zero income to receiving caregiver pay and don't report it, the system will eventually catch the discrepancy through data matching with the IRS or your employer's wage reports. At that point, you might owe back premiums or face a coverage gap.

Second, not claiming the 2014-7 exclusion on their tax return. If you qualify but file your taxes without the exclusion, your MAGI will be higher than it needs to be, and that inflated number is what Medicaid uses. A tax preparer unfamiliar with caregiver pay rules might not know about this exclusion. You may need to bring it up yourself. The rules around Medicaid waiver payment taxation are worth reviewing before tax season.

Third, counting household income incorrectly. Medicaid looks at household income for the people on the application, and household composition rules can be confusing. If you live with the care recipient and they're on a different Medicaid case, your income and theirs are usually calculated separately. But if you're on the same tax return as a spouse whose income also counts, the math changes. Getting financial help for caregivers often starts with making sure the numbers going into the system are correct.

How to Protect Your Coverage While Getting Paid

The practical steps here aren't complicated, but they do require you to be proactive.

Start by calling your state's Medicaid office (or your managed care plan's member services line) before your first caregiver paycheck arrives. Tell them you're about to start earning income through a Medicaid waiver program and ask specifically how that income will be counted. Get the answer in writing if possible, or at least note the date, time, and name of the person you spoke with.

Next, coordinate with your tax preparer. Make sure they understand IRS Notice 2014-7 and can confirm whether your specific payment arrangement qualifies. If you prepare your own taxes, IRS Publication 525 (the section on difficulty-of-care payments) walks through the exclusion. Apply it correctly the first time so your MAGI reflects your actual taxable income.

Finally, keep records. Save every pay stub, every W-2, every letter from your Medicaid office. If your eligibility is ever questioned, documentation is what resolves it. Caregivers who can show that their income was properly excluded under 2014-7 usually get their coverage reinstated without much difficulty. Those who can't produce records face a longer, harder process.

If you're trying to figure out how caregiver income affects Medicaid eligibility for your specific situation, Paid.care's qualification process includes guidance on income reporting and eligibility protection as part of getting you enrolled and paid.

Frequently Asked Questions

Does getting paid as a family caregiver through Medicaid automatically disqualify me from my own Medicaid coverage?

No. How caregiver income affects Medicaid eligibility depends on whether your pay qualifies for the IRS Notice 2014-7 exclusion and how your state counts that income. If you live with the care recipient and your pay comes through a Medicaid waiver program, the income may be excluded from your MAGI entirely, leaving your eligibility unchanged. Even without the exclusion, your total income has to exceed your state's threshold before coverage is affected.

Do I have to live with the person I'm caring for to get the tax exclusion?

Under IRS Notice 2014-7, yes. The exclusion applies to difficulty-of-care payments made under a Medicaid waiver program when the caregiver and care recipient live in the same home. If you provide care but live at a separate address, the exclusion generally doesn't apply, and your caregiver pay would be counted as taxable income. Some caregivers have rearranged living situations specifically to qualify, though you should get professional tax advice before making that decision.

What happens if I accidentally earn too much and lose Medicaid?

If your income exceeds Medicaid limits, your state will notify you that your coverage is ending, usually with a 30-day or 60-day advance notice. You'll typically have the option to apply for subsidized coverage through the ACA Marketplace during a special enrollment period triggered by the Medicaid loss. You can also appeal the Medicaid decision if you believe the income calculation was wrong. Reporting income changes promptly and accurately is the best way to avoid surprises.

Can my care recipient's Medicaid eligibility be affected by my caregiver income?

Generally, no. Your income as the caregiver is separate from the care recipient's Medicaid eligibility. The care recipient qualifies based on their own income, assets, and medical need. However, if you're a spouse providing care, spousal income rules apply under Medicaid's spend-down provisions, and the calculation gets more complicated. In most family caregiver arrangements where the caregiver is an adult child or other relative, the two cases are entirely independent.

Where can I check my state's current Medicaid income limits?

Your state's Medicaid agency website publishes current income limits, usually updated annually. For quick reference, Paid.care maintains guides for Indiana, Michigan, and other states that break down thresholds by household size and program type. These numbers change, so check them at least once a year, especially around open enrollment and tax season.