Caregiver Income and Disability Benefits: Which Programs Stack, Which Conflict, and How to Plan Around Both

Caregiver income and disability benefits can coexist, but only if you know which program you are on before your first paycheck arrives. SSDI, an earned benefit tied to your work history, leaves your check untouched as long as monthly countable earnings stay below the Substantial Gainful Activity threshold, which is $1,620 in 2026. SSI, a need-based program with a $2,000 resource limit, reduces your benefit on a roughly 50-cents-on-the-dollar formula and can suspend it entirely if accumulated wages push your bank balance over that ceiling at month's end. ABLE accounts protect SSI recipients by holding caregiver wages outside the resource count, and the IRS Notice 2014-7 exclusion can reduce taxable income for live-in caregivers paid through a Medicaid waiver. Getting the order of operations right, cash benefit first, then health coverage, then hours, is what separates families who keep both a paycheck and a benefit from those who trade one for the other.

If you collect SSI and start getting paid to care for your mom through a Medicaid waiver, your benefit check can shrink the very next month. If you collect SSDI instead, the same caregiver paycheck might not touch your benefits at all. That single difference, between SSI and SSDI, decides whether caregiver income and disability benefits stack neatly or collide hard, and most families don't find out until the reduction notice shows up.

So before you sign onto a paid caregiver program, you need to know which type of disability benefit you (or your loved one) actually receive, because the rules split sharply from there. This breakdown compares the two main disability programs head to head, shows where caregiver pay fits with each, and ends with a simple way to figure out what your own situation calls for.

The short version: SSDI is forgiving of caregiver wages up to a point, SSI is strict about every dollar, and Medicaid health coverage sits underneath both with its own asset and income tests. Get the order of operations right and you keep your benefits and your paycheck. Get it wrong and you trade one for the other.

The two disability programs caregiver income interacts with

Social Security runs two completely separate disability programs, and people mix them up constantly because both pay monthly and both involve the word "disability." They are not the same animal, and caregiver pay treats them differently.

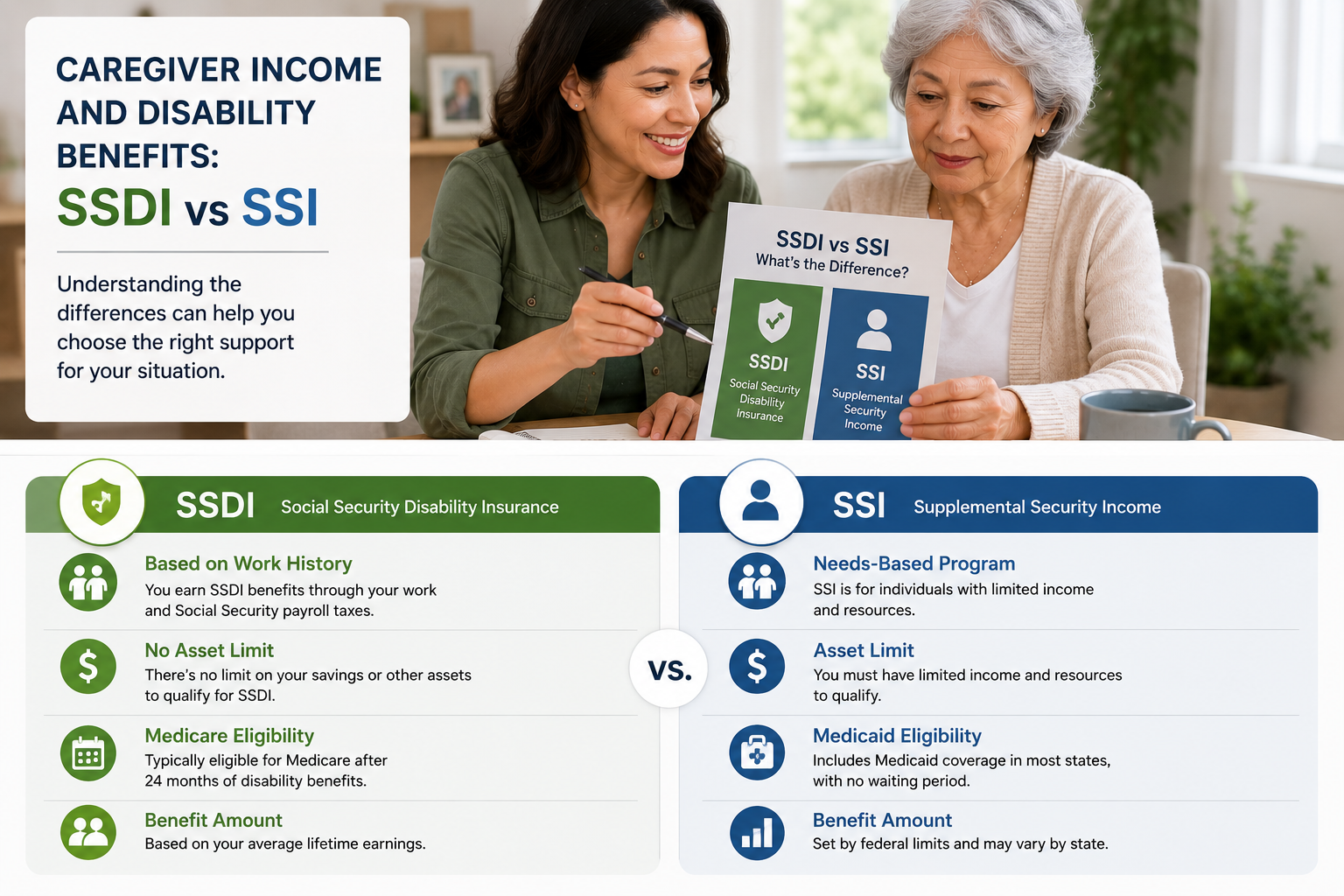

SSDI (Social Security Disability Insurance) is an earned benefit. You qualify because you worked, paid into Social Security through payroll taxes, and then became unable to work at a substantial level. Your benefit amount is based on your past earnings record, not your current bank balance. There's no asset limit. SSDI does not care if you own a house, have savings, or inherit money.

SSI (Supplemental Security Income) is a need-based benefit. You qualify because your income and resources are low, not because of your work history. In 2026 the resource limit is still $2,000 for an individual and $3,000 for a couple, and the program counts almost every source of income against your monthly payment. SSI is means-tested down to the dollar.

This matters for caregiver income and disability benefits specifically for a clear reason. A paid caregiver program, whether it's a Medicaid HCBS waiver, structured family caregiving, or a state home help program, pays you wages or a stipend. That payment is income. SSDI mostly ignores income below a work threshold. SSI counts it almost immediately. The same job, the same check, two opposite outcomes.

One more layer: many people on SSI also get Medicaid automatically, and many on SSDI get Medicare after a waiting period. So caregiver pay doesn't just affect the cash benefit, it can ripple into the health coverage tied to it. We cover that interaction in depth in how caregiver income affects your own Medicaid eligibility, and it's worth reading alongside this comparison.

How caregiver income affects SSDI

SSDI gives you the most room to earn caregiver wages without losing your benefit, and that's the headline most families need to hear. Because SSDI has no asset limit and no general income cap, your savings and your loved one's estate don't enter the picture at all. What SSDI watches is whether you're working at a level the agency calls Substantial Gainful Activity, or SGA.

For 2026, the SGA threshold for non-blind individuals is $1,620 per month in countable earnings (Social Security publishes this figure annually; it was $1,550 in 2024 and has risen with the cost-of-living adjustment). Earn below that consistently and your SSDI generally continues. Earn above it month after month, and Social Security may decide you're no longer disabled for program purposes.

Caregiver pay can push you over that line fast. Say a waiver approves you for 30 hours a week at $18 an hour. That's roughly $2,160 a month, well past the SGA threshold. So the planning question with SSDI isn't "will this disqualify me" in some vague sense, it's "how many hours can I be paid for before I cross SGA."

SSDI also offers cushions that SSI doesn't:

Trial Work Period: You get nine months (within a rolling 60-month window) where you can earn any amount and keep your full SSDI check. This lets you test paid caregiving without immediate risk.

Impairment-Related Work Expenses: Certain costs you need in order to work can be subtracted from your countable earnings, sometimes keeping you under SGA even when gross pay looks high.

Extended Period of Eligibility: After the trial work period, a 36-month stretch lets benefits reinstate in any month your earnings dip below SGA, without a new application.

If you're weighing part-time caregiving against your SSDI, the mechanics are spelled out further in our guide on whether working part-time affects disability benefits. The practical takeaway: SSDI recipients often take a capped number of caregiver hours on purpose, keeping monthly pay just under SGA so the benefit and the paycheck both keep coming.

How caregiver income affects SSI

SSI is where caregiver income gets dangerous if you walk in blind, because this program reduces your check almost dollar for dollar and enforces a hard $2,000 resource ceiling. Every choice you make about how you're paid matters here in a way it simply doesn't for SSDI.

SSI works on a monthly formula. The federal benefit rate sets your maximum payment, and Social Security subtracts your countable income from it. For earned income like caregiver wages, the agency disregards the first $65 (plus a $20 general exclusion in most cases), then counts roughly half of the rest against your benefit. So caregiver pay doesn't erase your SSI one for one, but it erodes it steadily, and enough hours will zero it out entirely.

Then there's the resource limit, which is the trap that catches more caregivers than the income rule. If your caregiver paychecks accumulate in a checking account and push your balance over $2,000 at the end of any month, SSI can suspend your benefit, even if your monthly income was fine. Money sitting still counts against you.

The income rule shrinks your SSI check. The resource rule can stop it cold. With caregiver pay, you have to manage both at once.

This is exactly where an ABLE account changes the math. ABLE accounts let people whose disability began before age 26 set aside savings that don't count toward the SSI $2,000 limit. Caregiver wages can be routed in, so your balance stays compliant while you still keep the money. We walk through the setup in using ABLE accounts to protect benefits while paying a family caregiver, and for SSI recipients specifically it's often the difference between keeping the benefit and losing it.

One bright spot: a payment type can sometimes sidestep the income hit entirely. Under IRS Notice 2014-7, certain Medicaid waiver payments to a caregiver living in the same home as the care recipient are excluded from federal income tax, and in some cases SSI treats them more favorably too. Whether that helps you depends on your living arrangement and your state. The deeper interaction is covered in will getting paid as a caregiver affect your disability benefits or SSI, which is the companion piece to this comparison and worth reading before you enroll.

Where Medicaid health coverage fits underneath both

Both disability programs often come bundled with health coverage, and caregiver income can shake that loose separately from the cash benefit, so you have to track it as its own risk. This is the layer families forget.

SSI recipients usually get Medicaid automatically. If caregiver pay reduces or ends your SSI, your Medicaid can be at risk too, unless your state has a protection that keeps it in place. Some states use a rule (often called 1619(b)) that lets you keep Medicaid even after earnings end your SSI cash benefit, as long as you're still under a state earnings threshold. Whether that applies to you depends on where you live, which is why Indiana, Michigan, and Illinois caregivers should each check their own state's specifics.

SSDI recipients typically get Medicare, not Medicaid, after a 24-month waiting period. Medicare has no asset or income test, so caregiver pay doesn't threaten it the way it threatens SSI-linked Medicaid. That's another reason SSDI recipients have more breathing room.

The wrinkle: caregiver pay flows through Medicaid waiver programs, and your loved one's Medicaid eligibility (the person receiving care) is a separate question from yours. The waiver pays you because they qualify. So you're managing potentially three eligibility tests at once, your cash benefit, your health coverage, and the care recipient's Medicaid. If you want to see how the whole funding mechanism works before you apply, our overview of how families get qualified and paid lays out the sequence.

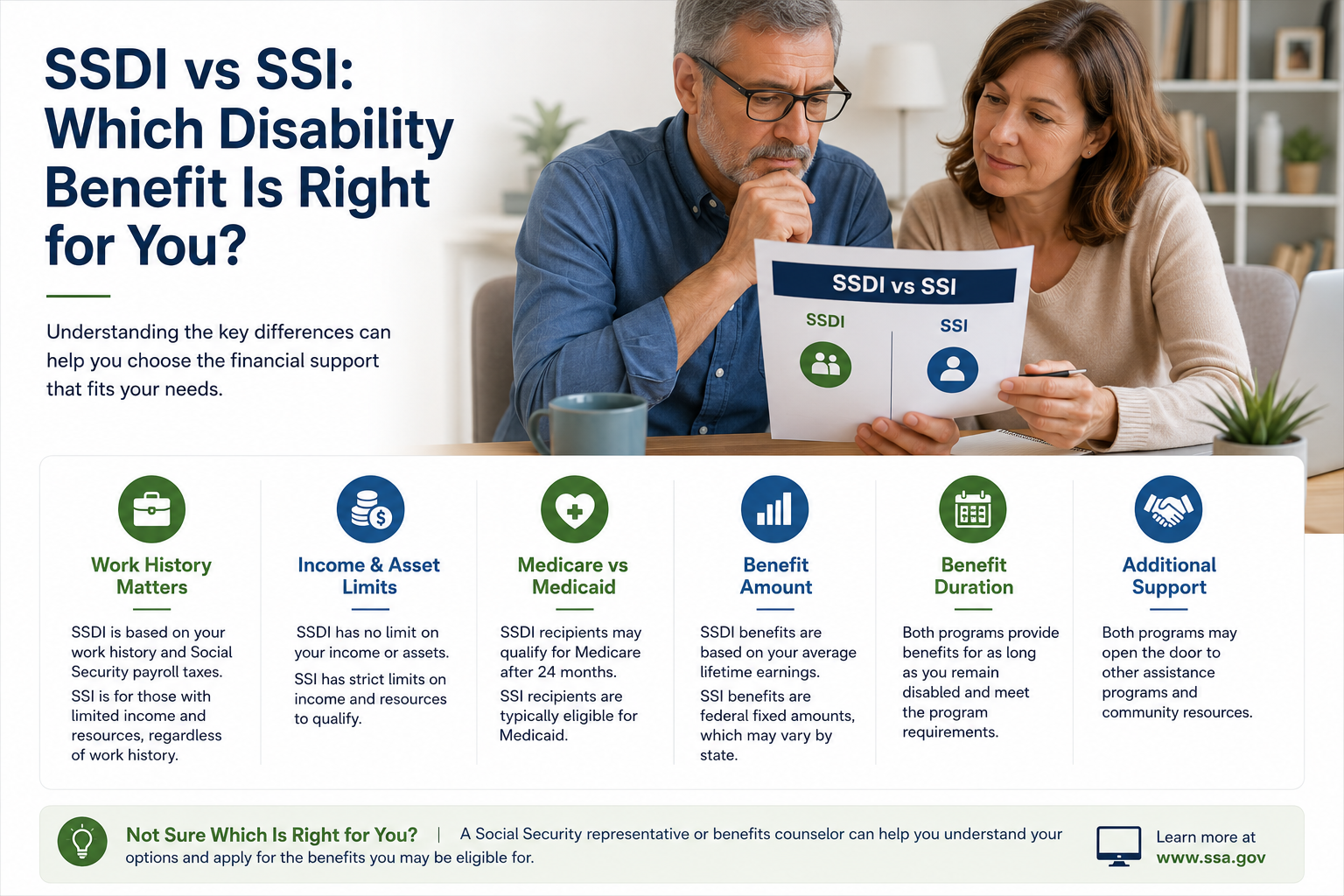

Comparing the two programs side by side

Here's the head-to-head on the criteria that actually decide whether caregiver income and disability benefits coexist or clash.

| Criterion | SSDI | SSI |

|---|---|---|

| What qualifies you | Work history and payroll-tax contributions | Low income and low resources |

| Asset / resource limit | None | $2,000 individual / $3,000 couple (2026) |

| How caregiver income is counted | Only matters if earnings cross SGA ($1,620/mo, 2026) | Reduces benefit on a roughly 50% formula after exclusions |

| Linked health coverage | Medicare after 24-month wait; not asset-tested | Medicaid, usually automatic; can be lost with the cash benefit |

| Built-in work protections | Trial Work Period, Extended Period of Eligibility | Earned income exclusions, ABLE accounts, possible 1619(b) Medicaid |

| Risk level from caregiver pay | Moderate, manageable by capping hours | High, requires active planning |

Read the table and the pattern jumps out. SSDI penalizes a level of work, so you manage it by watching one number each month. SSI penalizes income and accumulated money, so you manage it by controlling both the size of your check and where the money lands. For the broader picture of what you can earn beyond the paycheck itself, including tax exclusions and Social Security credits, see the financial benefits available to paid caregivers beyond the weekly check.

Which approach should you choose

The right move depends entirely on which benefit you receive and how many caregiver hours you're being offered. Use this as a decision guide.

- You're on SSDI and the program offers part-time hours: You likely keep both. Track your monthly countable earnings against the SGA figure and use the Trial Work Period to test paid caregiving with no immediate risk. Capping hours to stay under SGA is the standard play.

- You're on SSDI and offered near full-time hours: You may be better off treating caregiving as a return to work and letting the work-incentive rules carry you, rather than refusing hours. Run the numbers before deciding, because crossing SGA permanently is a real consequence.

- You're on SSI with any caregiver pay: Plan before your first check. Set up an ABLE account so wages don't blow past the $2,000 resource limit, understand the income reduction formula, and confirm whether your state protects your Medicaid if the SSI cash benefit ends. Do not enroll on autopilot.

- You're on SSI and the pay would zero out your benefit anyway: Sometimes the caregiver wage exceeds what SSI would have paid, making the trade worth it, but only if you've protected the Medicaid coverage underneath. That's the order: coverage first, then cash.

- You're not on disability but your loved one is: Their benefits and Medicaid drive the waiver that pays you. Your own income is a separate tax-and-budget question, walked through in financial planning for paid family caregivers.

One thing nobody should do is guess. The penalty for guessing wrong on SSI is a suspended check and possibly lost Medicaid. The penalty for guessing wrong on SSDI is a finding that you're no longer disabled. Both are reversible with effort, but both are painful, and both are avoidable with a short planning conversation before you enroll.

Frequently asked questions

Will getting paid as a caregiver automatically cancel my disability benefits?

No, caregiver income and disability benefits can coexist for most families with the right setup. On SSDI, your benefit continues as long as monthly countable earnings stay under the Substantial Gainful Activity threshold ($1,620 in 2026). On SSI, the benefit reduces gradually rather than vanishing, and tools like ABLE accounts keep you under the resource limit. The risk is real but manageable, the key is planning before your first paycheck rather than reacting to a reduction notice.

How do I know if I'm on SSDI or SSI?

Check your award letter or your Social Security online account. SSDI is based on your work record and has no asset limit, so if you qualified because of past employment, that's SSDI. SSI is need-based with a $2,000 resource cap, so if you qualified because of low income and limited savings, that's SSI. Some people receive both (called concurrent benefits), in which case both sets of rules apply at once and planning is especially important.

Does the IRS Notice 2014-7 tax exclusion also protect my SSI?

Not always, and the two are separate questions. Notice 2014-7 lets certain Medicaid waiver payments to a live-in caregiver be excluded from federal income tax. SSI uses its own income-counting rules, so a payment that's tax-free isn't automatically invisible to SSI. In some living arrangements the exclusion helps with both, but you should confirm your specific situation. The interaction between payment type and taxes is detailed in our breakdown of caregiver stipend versus caregiver wage and what each means for your taxes.

Can an ABLE account really protect my benefits while I earn caregiver pay?

Yes, for people whose disability began before age 26, an ABLE account is one of the strongest tools available. Money inside the account doesn't count toward the SSI $2,000 resource limit, so you can route caregiver wages in and keep your balance compliant. It doesn't change how income is counted in the month you earn it, but it solves the accumulation problem that suspends so many SSI checks. Setup details are in our guide on using ABLE accounts to protect benefits.

What if the caregiver pay is more than my disability check?

Then the trade can be worth it, but only after you protect the health coverage attached to the benefit. On SSI, the cash payment may be smaller than a full caregiver wage, so earning more makes sense, as long as you've confirmed your state keeps your Medicaid in place. On SSDI, full-time caregiving may move you off the disability rolls, which is a bigger decision because it affects your long-term status. Run both scenarios with someone who knows the rules before you commit.

The honest answer to most of these questions is that the right structure depends on your exact benefit, your state, and your hours, which is why guessing is the most expensive option. If you're in Indiana, Michigan, or Illinois and want help mapping caregiver income and disability benefits to your specific situation before you enroll, our free financial coaching and planning resources for paid family caregivers are built to do exactly that, so you keep your benefits and your paycheck instead of trading one for the other.