Tax Deductions and Credits Family Caregivers Can Claim in 2026

Family caregivers who spend their own money on a loved one's medical bills, housing, and daily needs can often recoup thousands at tax time, but most don't claim everything they're owed. The IRS offers several provisions that directly apply to your situation, and a handful of states add their own credits on top. Below is a ranked list of the most valuable tax deductions for family caregivers in 2026, ordered by potential dollar impact, with the criteria you actually need to meet.

Each item includes who qualifies, how much you can save, and the specific filing requirements. Some of these interact with your caregiver income and benefits, so pay attention to the interplay between deductions and any Medicaid or government program payments you receive.

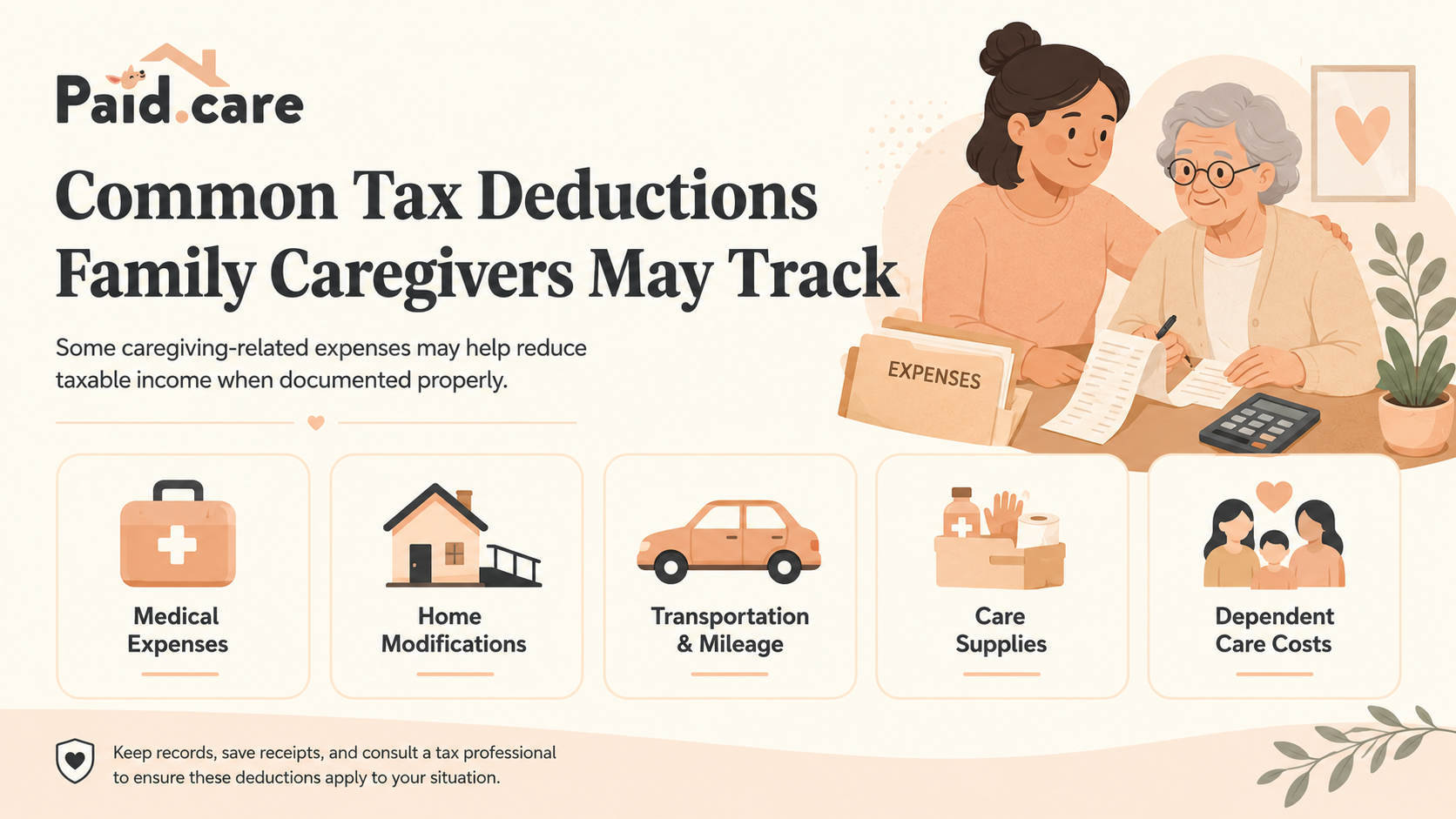

1. Medical Expense Deduction

This is the single largest tax break available to most family caregivers, and it's the one most people undercount. If you pay for a family member's medical care out of pocket, those expenses are deductible on Schedule A once they exceed 7.5% of your adjusted gross income (AGI). That threshold sounds steep, but caregiving costs add up fast: prescription copays, adult diapers, home health aide hours you paid privately, wheelchair ramps, medical transport, even certain home modifications prescribed by a doctor.

The key requirement is that you must be paying for someone who qualifies as your dependent or would qualify except that they earned too much income or filed a joint return. Your parent receiving Social Security doesn't automatically disqualify them. As long as you provide more than half of their total financial support, those medical expenses you cover are deductible on your return.

What Counts as a Medical Expense

The IRS defines medical expenses broadly under Publication 502. Doctor visits, hospital stays, lab tests, and prescriptions are obvious. Less obvious: the cost of installing grab bars, widening doorways for wheelchair access, or buying a hospital bed for home use. If a doctor prescribes it, the cost of in-home care (including personal care like bathing and dressing) qualifies too. Even mileage driven to medical appointments counts at the IRS medical mileage rate.

Keep every receipt. A shoe box of documentation is your best friend if you're ever questioned. If you're already receiving Medicaid waiver payments, those funds typically reimburse specific care costs rather than covering your out-of-pocket medical expenses, so there's often no double-dipping problem.

Potential savings: Varies widely, but caregivers who track everything often find $3,000–$8,000 or more in qualifying expenses. At a 22% marginal tax rate, that's $660–$1,760 back.

2. Dependent Care Tax Credit

If you pay someone to care for a qualifying dependent so that you (and your spouse, if filing jointly) can work or look for work, you may claim the Child and Dependent Care Credit on Form 2441. Despite the name, this credit isn't limited to children. It applies to a spouse or adult dependent who is physically or mentally unable to care for themselves and lives with you for more than half the year.

For 2026, you can claim up to $3,000 in care expenses for one qualifying person or $6,000 for two or more. The credit percentage ranges from 20% to 35% of those expenses, depending on your AGI. For most middle-income caregivers, the credit works out to 20%, which means up to $600 for one dependent or $1,200 for two.

A common mistake: assuming this credit only covers daycare for kids. If you hire a respite caregiver, a home health aide, or even a neighbor to watch your disabled parent while you go to work, those costs can qualify. The care provider just needs to report the income, and you need their taxpayer ID number. You can find more about respite care options and costs to understand what qualifies.

Potential savings: Up to $1,200 as a direct credit (dollar-for-dollar reduction of your tax bill, not just a deduction).

3. Credit for Other Dependents

Most caregivers know about the Child Tax Credit, but fewer realize there's a separate $500 nonrefundable credit for dependents who don't qualify as children under 17. If your elderly parent or disabled adult relative meets the IRS definition of a dependent, you can claim this credit directly on your 1040.

The dependency test is the same one used throughout this list: you must provide more than half of the person's total support for the year, they must be a qualifying relative (parent, grandparent, sibling, and several other relationships qualify), and their gross income must fall below the exemption amount (which is adjusted annually for inflation). Social Security benefits generally don't count as gross income for this test, which means many elderly parents qualify even though they receive monthly checks.

This credit phases out at higher incomes ($200,000 for single filers, $400,000 for married filing jointly), but most family caregivers fall well within those thresholds.

Potential savings: $500 per qualifying dependent, directly off your tax bill.

4. Head of Household Filing Status

Filing as Head of Household instead of Single gives you a larger standard deduction and more favorable tax brackets. For 2026, the difference in the standard deduction alone is typically several thousand dollars compared to Single status.

You qualify if you're unmarried (or considered unmarried under IRS rules), you paid more than half the cost of keeping up your home for the year, and a qualifying person lived with you for more than half the year. Here's where it gets useful for caregivers: your parent doesn't actually have to live with you to count. If you pay more than half the cost of maintaining their separate household (rent, utilities, groceries, property taxes), they can qualify you for Head of Household status even if they live in their own home or an assisted living facility.

This is probably the most overlooked filing advantage for family caregivers. Many people providing financial support to aging parents don't realize they can claim this status. Double-check with a tax professional, because the support test is specific: you need to account for all sources of your parent's support, including any government benefits they receive.

Potential savings: Typically $1,000–$2,500 in reduced taxes compared to filing as Single, depending on your income bracket.

5. State-Level Caregiver Tax Credits

Several states offer their own caregiver tax credits that stack on top of federal benefits. These vary significantly by state, and they change year to year, so checking your state's current tax code matters.

Examples Worth Knowing

Some states provide a flat credit for taxpayers caring for an elderly or disabled family member at home. Others offer credits tied to specific out-of-pocket expenses like home modifications or adult day care. A few states have created credits specifically for family caregivers who forgo outside employment to provide care. If you're a caregiver in Indiana, Michigan, or Illinois, check your state's Department of Revenue website for the latest qualifying criteria. You can also explore the 2026 guide to federal and state caregiver tax credits for a detailed breakdown by state.

One important note for caregivers receiving Medicaid waiver payments: some state credits have income or program-participation requirements that interact with your caregiver pay. If you're earning through a program like Structured Family Caregiving in Indiana or the Michigan Home Help program, you'll want to understand how those payments affect your eligibility for state credits.

Potential savings: Ranges from $200 to $1,500+ depending on the state and your specific situation.

6. Flexible Spending Account (FSA) for Dependent Care

If your employer offers a Dependent Care FSA, you can set aside up to $5,000 per year in pretax dollars to cover care expenses for a qualifying dependent. The tax advantage here is that the money comes out of your paycheck before federal income tax, Social Security tax, and Medicare tax are calculated. That triple tax savings makes a Dependent Care FSA more valuable dollar-for-dollar than many deductions.

You can use FSA funds to pay for adult day care, respite care, or a home aide who watches your dependent while you work. The same qualifying rules apply as the Dependent Care Tax Credit, and you can't claim both for the same expenses. Generally, the FSA is the better deal if your marginal tax rate is above 15%, but run the numbers for your situation.

One catch: FSA elections happen during open enrollment, usually in the fall. If you've recently become a caregiver, a qualifying life event (like a parent moving in with you) may allow a mid-year enrollment change. Check with your HR department.

Potential savings: $1,000–$2,000+ in combined federal and FICA tax savings on $5,000 of contributions.

7. Earned Income Tax Credit (EITC) Considerations

The EITC is a refundable credit designed for low-to-moderate-income workers, and it's worth mentioning because many family caregivers fall into qualifying income ranges, especially those who reduced their work hours to provide care. If you're earning caregiver income through a Medicaid program and your total earnings fall within the EITC thresholds, you may qualify.

Whether your caregiver pay counts as earned income for EITC purposes depends on how it's structured. W-2 wages from a fiscal intermediary or home care agency count. Certain Medicaid waiver payments that you elect to exclude from gross income under IRS Notice 2014-7 are trickier. If you exclude those payments from income, they may not count as earned income for EITC purposes, which could reduce your credit. This is an area where understanding the difference between 1099 and W-2 caregiver classification really matters.

Talk to a tax preparer who understands caregiver income. The wrong choice here can cost you hundreds or thousands.

Potential savings: Up to several thousand dollars for qualifying filers, depending on income and number of dependents.

8. Charitable Deduction for Donated Care Supplies

This one's small but real. If you donate medical equipment, mobility aids, or other care supplies to a qualifying nonprofit (say, after your loved one no longer needs a hospital bed or walker), the fair market value of those items is deductible as a charitable contribution on Schedule A. It won't change your life at tax time, but it adds up alongside the other deductions on this list.

You need a written receipt from the organization and, for items valued over $500, you'll need to file Form 8283. If you're looking for places to donate, organizations like those listed in our guide to free walkers and mobility aids for seniors often accept gently used equipment.

Potential savings: Modest, typically $50–$300, but every bit counts when you're itemizing.

How Medicaid Caregiver Payments Affect Your Taxes

If you're getting paid as a family caregiver through a Medicaid waiver program, you need to understand IRS Notice 2014-7. This notice allows certain Medicaid waiver payments to be excluded from gross income if you live with the person you care for. The exclusion applies to payments under Medicaid Home and Community-Based Services (HCBS) waiver programs, which cover programs in Indiana, Michigan, Illinois, and most other states.

When you exclude these payments from income, they don't show up on your tax return as earnings. That can reduce your overall tax liability, but it also affects your eligibility for credits that require earned income (like the EITC, discussed above). It can also affect your ability to contribute to an IRA, since IRA contributions require earned income.

You don't have to exclude the payments. It's an election. For some caregivers, especially those with low income from other sources, including the payments as income and then claiming credits against it produces a better outcome. This is the kind of decision where a guide to reporting caregiver stipends on state taxes can help you think through the tradeoffs.

If you're currently providing unpaid care and want to explore getting paid through Medicaid programs, you can see how the qualification process works at Paid.care.

Practical Steps to Maximize Your 2026 Tax Benefits

Knowing what's available is only half the work. Actually claiming these tax deductions for family caregivers in 2026 requires documentation and some planning throughout the year.

Track every expense in real time. A simple spreadsheet or note on your phone works. Record the date, amount, what it was for, and who it was for. Reconstructing twelve months of receipts in March is miserable and leads to missed deductions.

Keep medical receipts separate. Your loved one's medical expenses and your own are different pots for tax purposes. Don't mix them.

Run the dependent support test early. Add up everything you contribute to your family member's support (housing, food, medical, clothing, transportation) and compare it to what they receive from other sources. If you're close to the 50% threshold, adjusting your contributions before year-end can lock in dependency status.

Decide on the Notice 2014-7 exclusion before filing. If you receive Medicaid waiver payments and live with your care recipient, model both scenarios: excluding the income versus including it and claiming available credits.

Find a tax preparer who understands caregiver situations. Not every CPA or tax software handles these provisions correctly. A preparer familiar with caregiver budgeting and Medicaid income rules can save you more than their fee.

Frequently Asked Questions

Can I claim tax deductions for family caregivers in 2026 if I receive Medicaid waiver payments?

Yes, you can still claim most deductions and credits even if you receive Medicaid waiver payments. The medical expense deduction, dependent credits, and Head of Household status are all separate from how you earn your caregiver income. The main interaction happens with credits that require earned income (like the EITC), where your decision to include or exclude waiver payments from gross income under IRS Notice 2014-7 changes the math. Check with a tax professional to model both scenarios.

Do I need to itemize to benefit from these caregiver tax breaks?

Some of them require itemizing (medical expenses and charitable donations are on Schedule A), but several of the most valuable ones don't. The Credit for Other Dependents, Dependent Care Credit, EITC, and Head of Household filing status all work whether you itemize or take the standard deduction. Start with the non-itemized benefits, and only switch to itemizing if your total Schedule A deductions exceed the standard deduction for your filing status.

What documentation does the IRS need if I claim my parent as a dependent?

The IRS doesn't require you to submit proof with your return, but you need to have it ready if audited. Keep records showing you provide more than half your parent's total support: bank statements showing rent or mortgage payments you make on their behalf, grocery receipts, medical bills you paid, and any other support costs. Also keep records of their income sources (Social Security statements, pension statements) to show their gross income falls below the dependency threshold.

Can two siblings split the dependent claim for a parent they both support?

Yes, through a Multiple Support Agreement (Form 2120). If no single person provides more than 50% of a parent's support but two or more people together exceed that threshold, the siblings can agree on which one claims the dependent. The claiming sibling must have provided at least 10% of total support. This comes up frequently when siblings share caregiving responsibilities and costs. Only one person can claim the dependent in a given tax year.

Are caregiver stipends from state programs considered taxable income?

It depends on the program and your living situation. Payments through Medicaid HCBS waivers can often be excluded from gross income under IRS Notice 2014-7 if you live with the care recipient. Payments from other sources, like VA caregiver stipends or private-pay arrangements, typically are taxable. If you receive a W-2 or 1099, report it as income unless you qualify for the specific Medicaid waiver exclusion.