Paying Family Members for Caregiving: How to Get Paid to Care for Your Loved One

Key Takeaways

In 2026, many U.S. programs—especially Medicaid, HCBS waivers, VA benefits, and paid family leave—now allow certain family members to be paid caregivers, but rules vary widely by state and program.

Most formal paths to get paid run through state Medicaid home and community based services and consumer directed programs. Practical next steps include calling your state Medicaid office or starting eligibility screening with Paid.care if you live in Indiana, Michigan, or Illinois.

Long-term care insurance, personal care agreements, and employer paid family leave can also compensate family caregivers, but each has strict eligibility and documentation requirements.

Not every caregiver will qualify for pay. However, using the right mix of state benefits, VA programs, and employer supports can significantly reduce the financial strain of caregiving.

Paid.care is a free, tech-enabled partner that helps caregivers in Indiana, Michigan, and Illinois understand options, complete paperwork, receive training, and get weekly payments when they qualify.

Introduction: Can Family Caregivers Really Get Paid in 2026?

Picture this: You’re an adult child in Michigan who just reduced your work hours to care for your mom, who has Alzheimer’s disease. The bills keep coming, but your paycheck shrinks. You’re not alone—millions of informal caregivers face this exact pressure every day.

Here’s the good news: Yes, it is often possible to get paid to care for a loved one. But only through specific channels:

Paid family leave laws in certain states

Long-term care insurance policies

Private personal care agreements

Every option has its own rules about who can be paid (spouse vs. adult child vs. friend), what tasks are covered (personal care vs. homemaker services like meal preparation), and how much they pay—often tied to local home care wage rates.

Paid.care focuses on helping family caregivers in Indiana, Michigan, and Illinois tap into state Medicaid programs and related payment pathways. This article walks you step-by-step through each major way to get compensated, no matter where you live.

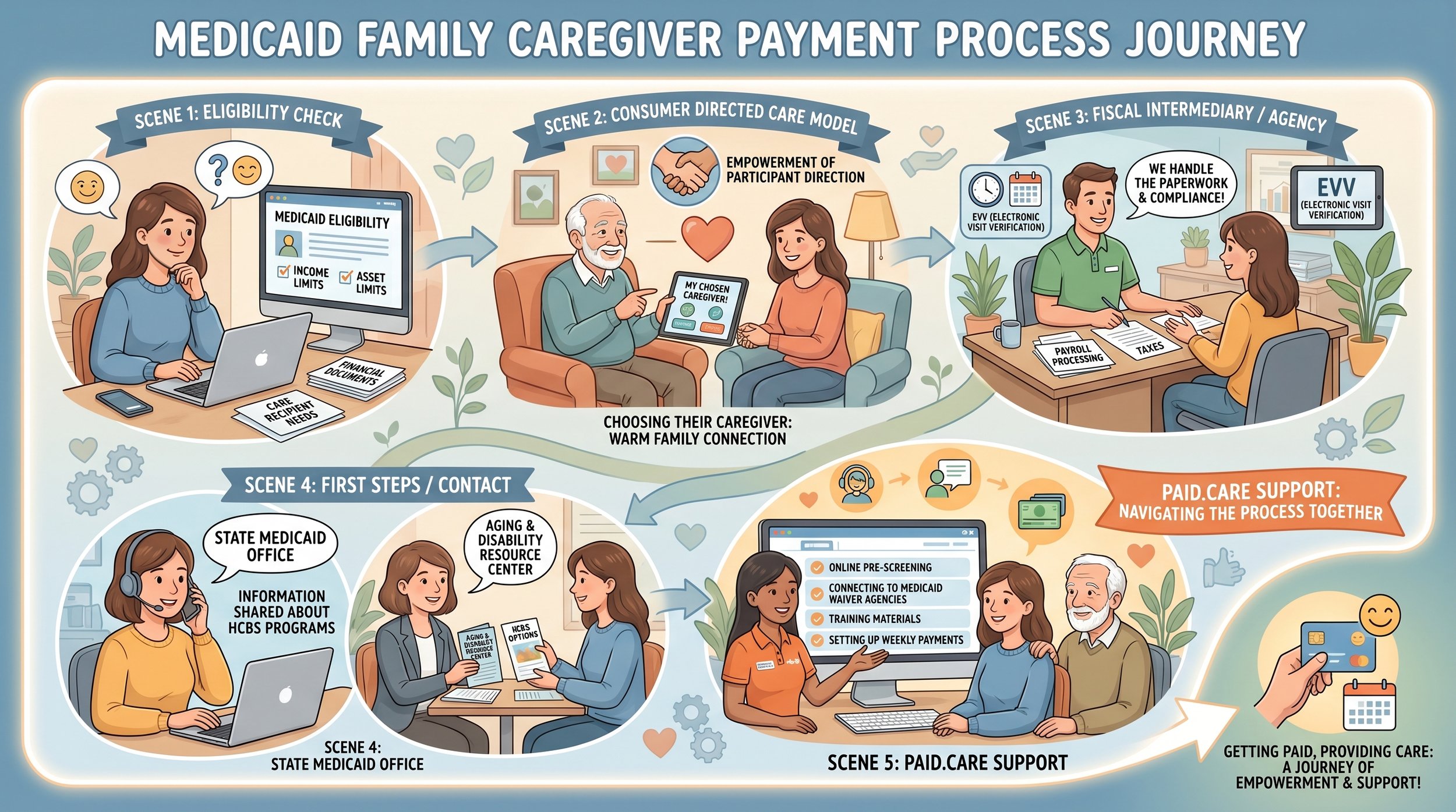

How to Get Paid by Medicaid as a Family Caregiver

Medicaid is a joint federal-state program that funds in-home care for low-income older adults and disabled individuals. Through home and community based services waivers and self directed care models, many states now pay family members to provide personal care services instead of placing recipients in a nursing home or assisted living facility.

As of 2026, most states allow some family members to become a paid caregiver through Medicaid personal care or attendant care programs. However, eligibility requirements, which relatives qualify (some states exclude spouses), and hourly rates all vary by state.

Financial eligibility basics:

Income limits often hover around 300% of the Federal Benefit Rate (roughly $2,829 monthly for individuals in 2026)

Asset limits typically range from $2,000 to $3,000 for single applicants

“Spend-down” rules may require excess assets to be depleted on medical needs before approval

Indiana’s Aged and Disabled Waiver, Michigan’s MI Choice, and Illinois’ Community Care Program each have specific thresholds—check current state Medicaid sites for exact figures

How consumer directed care works:

Under participant direction or self direction models, the care recipient (or their representative) can choose their caregiver. This often includes an adult child, sibling, or friend. A fiscal intermediary or agency handles payroll, taxes, and compliance—including electronic visit verification (EVV) systems required since 2019.

Your first steps:

Contact your state Medicaid office, local Aging and Disability Resource Center (ADRC), or Area Agency on Aging. Ask specifically about “self-directed” or “participant-directed” HCBS programs that pay family caregivers.

If you live in Indiana, Michigan, or Illinois, Paid.care can pre-screen your eligibility online, connect you to appropriate Medicaid waiver agencies, provide required training, and set you up for weekly payments once approved.

Steps to Become a Paid Family Caregiver Through Medicaid

While each state’s application process differs, most follow a similar sequence you can plan around:

Confirm apparent eligibility – Verify the Medicaid recipient appears financially and medically eligible for long-term care. They typically need help with at least two activities of daily living such as bathing, dressing, or mobility.

Submit a Medicaid application – File with the correct state office, including financial documentation, medical records, and proof of citizenship or residency.

Request HCBS waiver enrollment – Specifically ask for a home and community based services waiver or personal care program allowing consumer direction.

Complete the in-home assessment – A nurse or case manager evaluates the care recipient’s needs and determines how many hours of care are authorized weekly.

Designate your caregiver role – Complete required forms, pass background checks, and finish any online or in-person training modules (often 10-40 hours depending on the state).

Begin logging hours – Use an EVV system or mobile app to track shifts. Paid.care offers an app for caregivers in Indiana, Michigan, and Illinois to log hours and receive weekly payment.

Important notes:

In some states, spouses cannot be paid under certain Medicaid programs; in others, they can. Check your state’s current 2026 rules.

Realistic timelines run from several weeks to a few months from first application to first paycheck.

HCBS waivers may have waitlists—over 700,000 people nationally were waiting for waiver slots per 2025 HHS data.

Getting Paid to Care for a Veteran: Key VA Programs

The U.S. Department of Veterans Affairs offers multiple benefit streams that can financially support a family caregiver of an eligible veteran or surviving spouse. Here are four major pathways:

Aid and Attendance (A&A)

A pension add-on for wartime veterans or surviving spouses who need help with daily living activities. Benefits can reach up to $2,727 monthly for a single veteran in 2026. Funds can be used to pay a family caregiver via a private agreement.

Housebound Benefits

An increased pension (up to $2,055 monthly) for veterans substantially confined to their home. While not a direct stipend, these funds help offset family caregiving costs.

Program of Comprehensive Assistance for Family Caregivers (PCAFC)

This program pays monthly stipends averaging $2,000-$3,000 to the primary caregiver of qualifying post-9/11 and certain pre-9/11 veterans with serious injuries. Benefits include training, 30 days respite care, counseling, and CHAMPVA health coverage. Spouses are often eligible as primary caregivers.

Veteran Directed Care (VDC)

Available at 50+ VA sites nationally, VDC provides a flexible budget ($1,500-$4,000 monthly) for veterans needing nursing home-level care. Veterans can hire relatives (non-spouses in some cases) at local market rates.

Getting help navigating VA benefits:

Eligibility depends on service period, disability ratings, functional needs, and income. Work with a VA social worker, Veterans Service Organization (VSO) like the American Legion, or nonprofits like the Elizabeth Dole Foundation.

VA benefits can sometimes layer with Medicaid, but families should get professional advice before combining programs to avoid “double-dipping” scrutiny.

Paid Family Leave: Getting Short-Term Income While You Provide Care

Paid family leave is fundamentally different from Medicaid or VA programs. It replaces a portion of a worker’s wages for a limited time so they can step away from employment to care for a family member.

As of 2026, 13 states plus Washington, DC have mandatory paid family leave laws. Benefits typically replace 60-90% of wages, with weekly caps often ranging from $800-$1,300. Durations commonly span 4-12 weeks.

Who might qualify:

Employees in states with paid family leave laws who meet prior earnings thresholds

Self-employed workers who opt into voluntary paid leave insurance (available in some states)

Workers whose employers offer separate caregiver leave policies, even without state mandates

The typical process:

Check your state labor department website and employer HR policy

Notify your employer according to required timelines

Gather medical certification showing your family member’s serious health condition

Submit a claim through the state benefits system or employer administrator

Await approval (often 1-3 weeks)

Reality check: Paid family leave provides temporary income—usually weeks, not months or years. It bridges the gap while families apply for Medicaid, VA benefits, or long-term care insurance claims. It’s not a long-term caregiving wage.

Indiana, Michigan, and Illinois do not currently have mandatory state paid family leave programs. Residents should check employer policies and note that employers partnering with Paid.care can offer additional support to employee-caregivers.

Long-Term Care Insurance and Personal Care Agreements

Long-Term Care Insurance (LTCI)

Long-term care insurance is a private policy that pays for services like nursing home care, assisted living facility stays, and in-home personal care. Only 7-10 million Americans hold these policies due to high premiums ($3,000-$5,000 annually).

How LTCI might pay family caregivers:

Some policies explicitly allow benefits for informal caregivers, including family

Many policies require caregivers to be licensed or agency-affiliated—Paid.care’s partner agencies may satisfy this requirement

Triggers typically include needing help with 2+ ADLs or cognitive impairment

Action steps: Locate the original policy, contact the carrier, and request written confirmation of whether family caregiving at home qualifies under the policy’s terms.

Personal Care Agreements

A personal care agreement (also called a caregiver contract) is a written, legally binding document between a care recipient and loved one’s caregiver. It specifies duties, hours, and hourly pay at reasonable local market rates (typically $18-$25/hour based on Genworth surveys).

Why this matters:

Formalizes pay so payments appear as compensation for services, not gifts

Critical for Medicaid’s 5-year look-back and asset-transfer rules

Helps document legitimate “spend-down” for Medicaid planning

Essential elements:

Detailed description of caregiving duties

Market-rate hourly pay based on local data

Payment schedule (contemporaneous, not lump-sum)

Doctor’s letter confirming care needs

Signed before services begin

Families expecting to apply for Medicaid within a few years should consult an elder law attorney to draft or review any caregiver agreement. Improper documentation can trigger gift penalties or disqualify applicants.

State Agencies, Area Agencies on Aging, and Local Support

Many caregivers never learn about paid caregiving options because government programs are fragmented across agencies. Local aging organizations often serve as the “front door” into the system.

What Area Agencies on Aging (AAAs) and ADRCs offer:

Counseling on long-term care options

Screening for HCBS waivers, respite care vouchers, and caregiver support grants

Application assistance for Medicaid and other programs

Information about adult day care, adult foster care, and structured family caregiving options

Finding your local AAA:

Search your ZIP code alongside “Area Agency on Aging” or call the Eldercare Locator at 800-677-1116. The Administration for Community Living maintains national directories.

Even if you don’t qualify for Medicaid, AAAs may help locate respite vouchers, sliding-scale home care, or training programs that reduce financial strain.

Indiana, Michigan, and Illinois residents should both contact their local AAA/ADRC and check with Paid.care—we coordinate with agencies and Medicaid waiver providers to streamline your path to becoming a paid family caregiver.

Where Paid Caregiving Programs Fall Short—and How Paid.care Helps

Let’s be honest: Even in 2026, many family caregivers won’t qualify for any direct paycheck. Income levels, program waitlists, relationship restrictions, or medical criteria can disqualify both you and your loved one.

Common barriers:

Complex, confusing application processes for Medicaid and VA benefits

Long waitlists for HCBS waiver slots (months to years in high-demand states)

Limited authorized hours that cap monthly payments at $1,500-$3,000

Training mandates and EVV compliance requirements

Spouse exclusions in roughly 20+ states

What Paid.care offers in Indiana, Michigan, and Illinois:

Free eligibility screening for Medicaid and related programs

Care coaching and required training to meet program standards

A mobile app to track shifts, log EVV, and manage schedules

Weekly payments processed through partner agencies once approved

Paid.care is not an insurance company or law firm. We’re a tech-enabled services platform that connects unpaid caregivers to government programs that can pay them for work they’re already doing.

Ready to find out if you qualify? If you’re in Indiana, Michigan, or Illinois and already helping an elderly or disabled loved one, complete an online eligibility check or speak with a Paid.care care coach today.

FAQs

-

Pay rates depend on the program and local market wages. Medicaid HCBS programs often pay near the local home care aide rate—roughly $16-$22 per hour as of 2025-2026, with Midwestern states typically in the $17-$20 range. Total monthly income equals your hourly rate times authorized hours (often 10-50 weekly), not necessarily total hours you informally provide. Paid.care shares current typical ranges for Indiana, Michigan, and Illinois during eligibility screening.

-

In most cases, yes—payments are treated as taxable W-2 income. However, special rules like “difficulty of care” exclusions may apply when the caregiver lives with the care recipient. Keep detailed records and consult a tax professional or IRS guidance. Paid.care and partner agencies issue appropriate tax forms so taxes are handled correctly.

-

It depends on the specific program and state. Some Medicaid HCBS waivers allow spouse pay; others don’t. VA’s PCAFC often allows spouses as primary caregivers. Paid family leave laws typically cover caring for a spouse. Check your state’s current 2026 rules—Paid.care clarifies spouse eligibility for programs in Indiana, Michigan, and Illinois during screening.

-

Consider these alternatives:

Explore paid family leave or employer caregiver benefits for short-term support

Check long-term care insurance for family care coverage

Draft a personal care agreement using private funds with an elder law attorney

Contact your AAA for respite vouchers, grants, or sliding-scale care

Claim tax credits like the dependent care credit (up to $3,000 maximum)