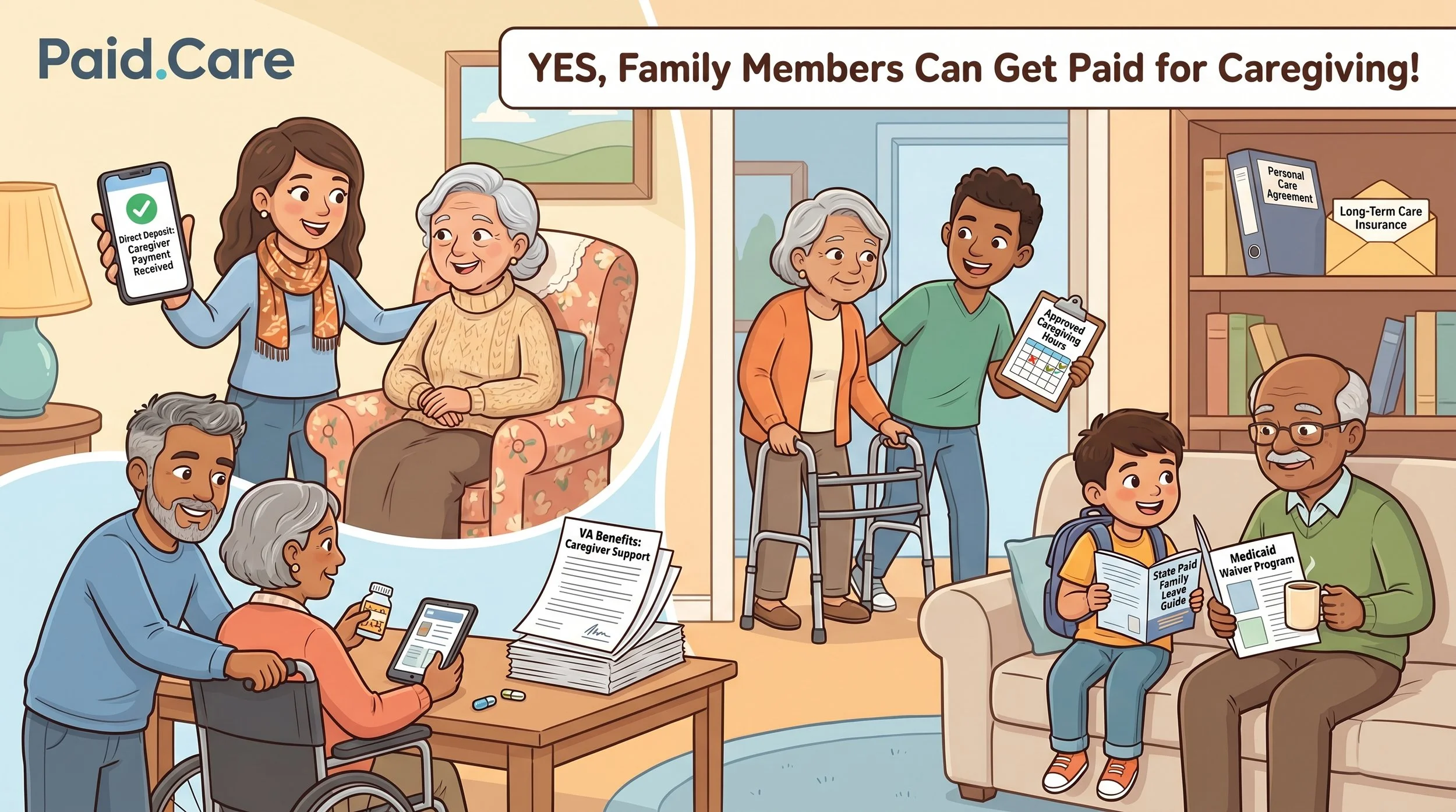

Can Family Members Get Paid for Caregiving?

Key Takeaways

Yes, family members can get paid for caregiving through Medicaid Home and Community Based Services waivers, consumer directed personal assistance programs, Veterans Affairs benefits, paid family leave, and private arrangements.

Eligibility requirements, hourly pay rates, and which relatives qualify depend on your state, the specific program, and the amount of your loved one’s income, assets, and care needs.

In Indiana, Michigan, and Illinois, programs like structured family caregiving and other Medicaid waivers often allow relatives—including an adult child—to become a paid caregiver.

Paid.care helps families in these states check eligibility, complete applications, get trained, and receive weekly payments through a mobile app.

This article walks through each major option step-by-step and ends with a FAQ covering taxes, live-in rules, and combining government programs.

Can Family Members Get Paid for Caregiving at All?

Yes, but it depends on your state, the program, and your loved one’s situation. As of 2025–2026, multiple pathways exist for family members to receive financial compensation for providing care.

A family caregiver is typically an unpaid relative or close friend who provides daily help at home with activities of daily living like bathing, dressing, meal preparation, giving medicine, and mobility assistance.

The main pathways for payment include:

Medicaid home care and waiver programs

VA caregiver programs (for qualified veterans and surviving spouses)

State paid family leave programs

Long-term care insurance reimbursement

Private personal care agreements

One important clarification: traditional Medicare generally does NOT pay family members directly for caregiving—a common misconception many caregivers discover too late.

Getting Paid as a Family Caregiver Through Medicaid

Medicaid is a joint federal–state health coverage program for low-income and disabled individuals. Because rules differ by state, what works in one location may not apply in another.

Many states run Home and Community Based Services waivers and consumer directed programs that let the care recipient choose and pay a relative as a caregiver. All 50 states and the District of Columbia offer some type of Medicaid-funded consumer-directed personal care assistance program, allowing family members to be paid caregivers.

Personal care services that can typically be paid include:

Help with bathing, dressing, and toileting

Meal preparation and feeding assistance

Medication reminders

Light housekeeping and homemaker services

Supervision for safety (for those with Alzheimer’s disease or cognitive impairment)

Spouses are sometimes excluded in certain waivers, while adult children, siblings, and even friends are more commonly allowed. For example, in Michigan, an adult daughter earned $17/hour for 40 weekly hours helping her mother through the MI Choice waiver after a dementia assessment confirmed nursing home level needs.

The compensation rates for family caregivers under Medicaid programs typically range from $13 to $18 per hour, depending on the state and the going rates for home care aides.

Steps to Become a Paid Family Caregiver Through Medicaid

The process to become a paid family caregiver varies by state, but these general steps apply across most state Medicaid programs:

Step 1: Confirm that the care recipient is eligible for Medicaid (income, assets typically under $2,000, disability or age 65+, state residency) and, if not enrolled, apply through your state’s Medicaid portal or local office.

Step 2: Ask specifically about Home and Community Based Services waivers or consumer directed personal assistance programs that allow hiring a family member as a paid caregiver.

Step 3: Request a functional needs assessment (often done by a nurse or social worker) that documents help needed with Activities of Daily Living and Instrumental Activities of Daily Living. The care recipient must be assessed as requiring assistance with daily living activities.

Step 4: Once approved, identify whether the state uses an agency model (you become an employee of an agency) or a self-directed model (the loved one or representative hires you with Medicaid funds).

Step 5: Complete required onboarding: paperwork, background checks, training, and timesheet setup. To become a paid caregiver, individuals often need to meet specific training and certification requirements set by their state, which may include background checks.

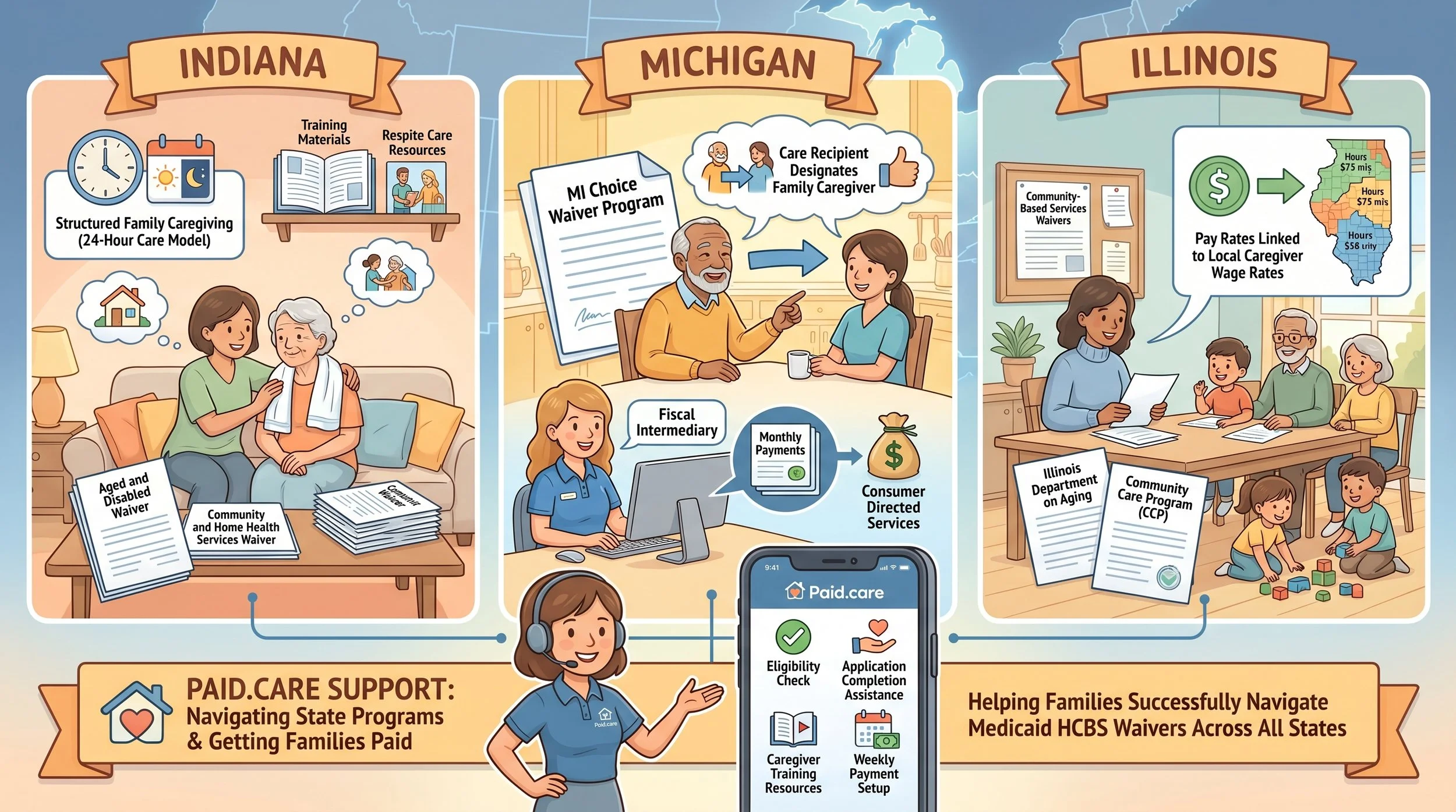

Medicaid Options in Indiana, Michigan, and Illinois (Where Paid.care Operates)

In Paid.care’s active states, all three use Medicaid HCBS waivers and structured programs that can compensate family caregivers.

Indiana: The Aged and Disabled Waiver and Community and Home Health Services Waiver can allow relatives to be paid. As of October 2022, seven states offer Structured Family Caregiving through Medicaid, including Connecticut, Georgia, Indiana, Louisiana, Missouri, North Carolina, and South Dakota. Structured family caregiving allows family caregivers to be paid for providing 24-hour care and assistance with daily personal care needs, such as bathing and dressing, to individuals who are Medicaid eligible. In these programs, caregivers may receive training and respite care, and the care recipient must meet specific eligibility requirements set by the state Medicaid agency.

Michigan: MI Choice and similar waivers support consumer directed services where a loved one designates a family member varies as their caregiver and a fiscal intermediary manages monthly payments.

Illinois: The Illinois Department on Aging and community based services waivers allow family caregivers under programs like the Community Care Program, with pay linked to local caregiver wage rates.

Paid.care helps families in these states check eligibility, complete applications, handle caregiver training, and get set up with weekly payments via a mobile app.

Getting Paid as a Family Caregiver Through Veterans Affairs (VA) Programs

U.S. veterans and some surviving spouses may qualify for VA-funded caregiver compensation or stipends. Several distinct programs exist, each with its own rules and application process.

Major VA-related caregiver payment paths include:

Aid and Attendance pension supplement

Housebound benefits

Program of Comprehensive Assistance for Family Caregivers (PCAFC)

Veteran-Directed Care (VDC)

Benefits can come as a cash monthly VA pension supplement, a monthly caregiver stipend, or a flexible budget to hire a loved one’s caregiver. Working with a VA-accredited representative or Veterans Service Organization can help avoid missed benefits and delays.

Key VA Programs That Can Pay Family Caregivers

Aid and Attendance: An extra monthly amount (typically $1,000–$2,500) added to the VA pension for veterans or surviving spouses needing help with ADLs. This can fund payment to a family member under a written care agreement. For example, a Texas daughter received $1,200/month supplement for her father’s bathing and mobility help.

Housebound benefit: An additional pension amount ($900–$1,800) for veterans largely confined to their home, sometimes combined with private caregiver payment arrangements for the veteran’s home care needs.

Program of Comprehensive Assistance for Family Caregivers (PCAFC): This program provides a monthly stipend, health insurance (CHAMPVA), and training to a designated primary caregiver of an eligible veteran with serious service-connected disabilities. The Program of Comprehensive Assistance for Family Caregivers provides a monthly stipend to caregivers of veterans with a service-connected disability rating of 70% or higher.

Veteran-Directed Care (VDC): Veteran-Directed Care allows veterans a flexible budget to hire caregivers, including family members. Allocates $2,000–$4,000 monthly for self-hiring through local area agencies on Aging and Disability.

Steps to Become a Paid Family Caregiver Through the VA

VA processes can be complex and paperwork-heavy. Patience and documentation are essential.

Step 1: Ensure the eligible veteran is enrolled in VA health care and receiving any applicable VA pension or disability benefits.

Step 2: Schedule an appointment with a VA social worker or Veterans Affairs benefits counselor to review whether PCAFC, VDC, Aid and Attendance, or Housebound benefits fit the veteran’s care situation.

Step 3: Gather medical records, service records (DD Form 214), and evidence of daily care needs.

Step 4: Complete program-specific applications, including naming the family caregiver where required.

Step 5: Follow up on decisions, respond promptly to VA requests, and attend any required caregiver training or orientation sessions.

Getting Paid for Caregiving Through State Paid Family Leave

Paid family leave is a state-mandated program that replaces a portion of a worker’s wages while they take time off to care for a seriously ill family member. Paid family leave laws in certain states allow workers to receive partial wage replacement while caring for a relative.

PFL differs from Medicaid or VA programs: it pays the worker (caregiver) for a limited time but does not fund ongoing long-term health care.

As of 2025–2026, just over a dozen states plus Washington, DC offer family leave programs with paid benefits. California, New York, and New Jersey have some of the most established programs. California’s program paid an average of $950/week for 8 weeks in 2024.

Eligibility, leave duration (typically 6-12 weeks), covered relationships, and wage replacement percentages vary widely by state. Self-employed workers may need to opt into voluntary coverage.

Steps to Access Paid Family Leave as a Caregiver

Coordinate with your employer’s HR department early to understand your options for unpaid leave under FMLA and any state-mandated paid family leave program.

Step 1: Check your state’s official paid family leave website to see if benefits exist and whether your employer is covered.

Step 2: Review your employer’s policies, waiting periods, and whether they offer family leave programs that coordinate with federal protections.

Step 3: Work with your loved one’s health care provider to obtain medical certification forms documenting the serious health condition.

Step 4: Submit the state or insurer application, attach medical certifications, and keep copies of everything.

Step 5: Once approved, plan your leave schedule (continuous or intermittent) and track your benefits start date, weekly benefit amount, and end date.

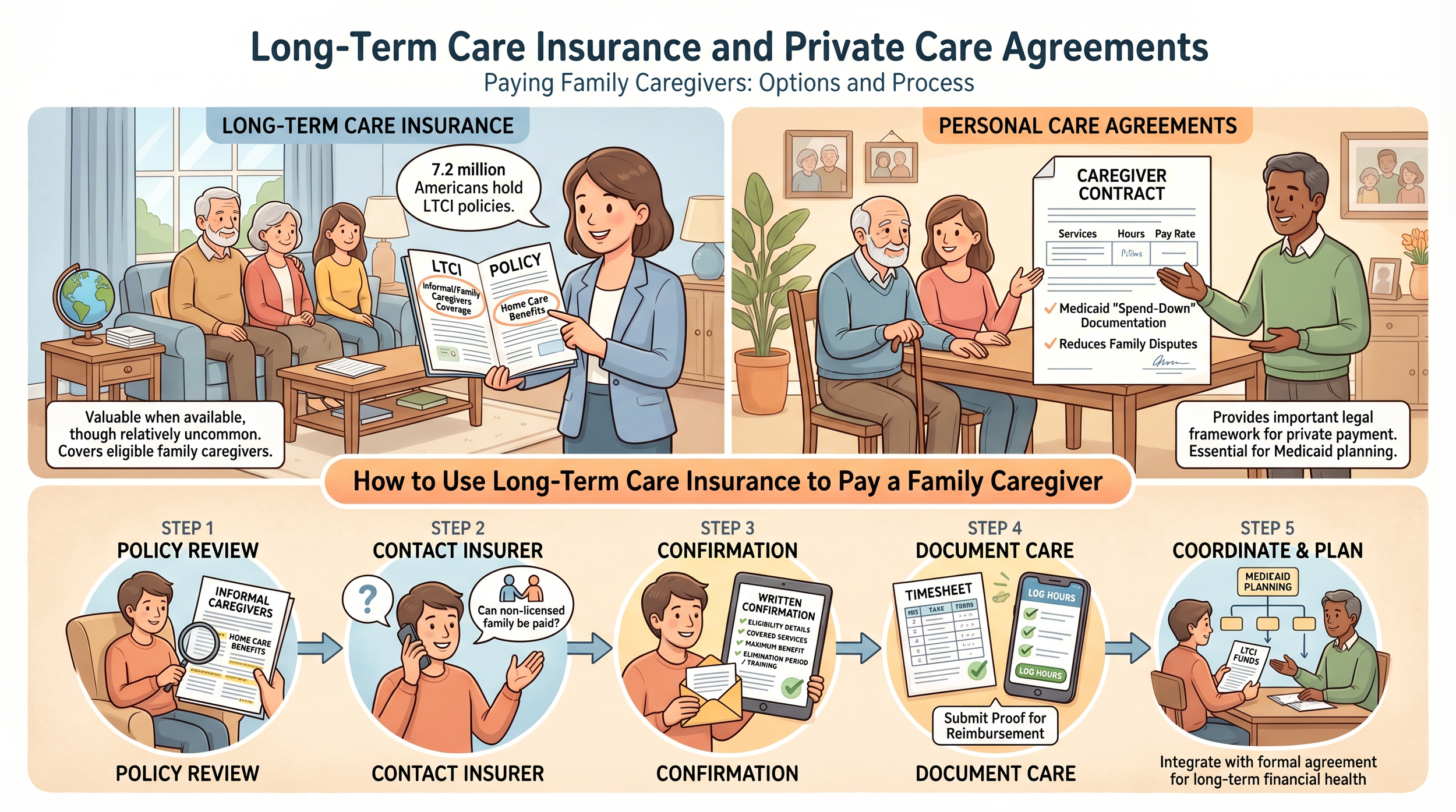

Long-Term Care Insurance and Private Care Agreements

Some families pay family members privately using long-term care insurance benefits or out-of-pocket funds.

Long-term care insurance is relatively uncommon—only about 7.2 million Americans hold policies—but when available, it may cover in-home care by a family member if policy rules allow. Long-term care insurance policies may allow family members to be compensated for caregiving, but this varies by policy and requires confirmation from the insurance provider.

A personal care agreement (caregiver contract) is a written document between the care recipient and family caregiver stating services, hours, and pay rate. Such agreements help document legitimate payments for Medicaid “spend-down” and reduce disputes among relatives about financial assistance.

Consulting an elder law attorney or financial planner when drafting a care agreement is advisable, especially if large sums or estate implications are involved.

How to Use Long-Term Care Insurance to Pay a Family Caregiver

Each LTCI policy is unique, so details must be verified in writing.

Step 1: Locate the full LTCI policy and review sections on “informal caregivers” or “family caregivers” and home care benefits.

Step 2: Call the insurance agent or insurer and ask specifically whether a family member who is not a licensed nurse can be paid.

Step 3: Request written confirmation of eligibility, covered services, maximum daily or monthly benefit amounts, elimination periods, and any training requirements.

Step 4: Set up a system to document hours and tasks performed using timesheets or an app, and submit required proof for reimbursement.

Step 5: Coordinate with an attorney if using LTCI funds within a formal personal care agreement for Medicaid planning purposes.

How Paid.care Helps Family Caregivers in Indiana, Michigan, and Illinois

Paid.care’s mission is helping unpaid family caregivers in Indiana, Michigan, and Illinois get qualified, trained, and paid through Medicaid-funded home care programs.

As a tech-enabled services platform, Paid.care supports caregivers and care recipients throughout the process: checking Medicaid waiver eligibility, completing applications, and coordinating required assessments. Many caregivers appreciate the care coaching and financial coaching services that help manage both the emotional load of caregiving and practical budgeting concerns.

The mobile app tracks caregiving hours and shifts, and ensures weekly payments once the caregiver is properly enrolled and approved—no waiting for monthly payments.

If you’re caring for an elderly or disabled loved one in Indiana, Michigan, or Illinois, check your eligibility with Paid.care to see if you can become a paid family caregiver.

Limitations, Tax Considerations, and When Payment May Not Be Possible

Despite multiple programs, many caregivers will not qualify for formal pay.

Common barriers include:

Loved one not meeting financial requirements for Medicaid

State waivers closed or with long waitlists (exceeding 700,000 nationally)

Excluded caregiver relationships (some states exclude spouses or legal guardians)

Care recipient not meeting the following criteria for nursing home level care

Lack of required documentation of care needs

Tax considerations: Income from caregiving programs is generally taxable, though there are exceptions under IRS guidelines. Caregivers may receive a W-2 or 1099 depending on the arrangement. Some states offer “difficulty of care” income exclusions—consult a tax professional for personalized advice. Tax credits may also apply in certain situations.

Being a paid caregiver can affect eligibility for means-tested benefits like SNAP or SSI, so families should review potential impacts with care referrals to local experts.

FAQs

-

Some Medicaid and VA programs allow live-in family caregivers to be paid, while others restrict or reduce payment if rent and utilities are already provided. Rules vary by state—some HCBS waivers have specific “live-in caregiver” policies that affect hours or reimbursement. In about 30 states, Medicaid reduces pay 25-50% for shared housing. Ask directly whether live-in status changes eligibility before signing any agreement.

-

Yes, in some cases. You must have enough available hours to provide care and document the approved work varies by program. State paid family leave usually requires taking time off from work, while Medicaid caregiver roles may be performed outside standard hours if the care plan allows. Paid.care can help you understand realistic schedules and income expectations.

-

You usually cannot be paid twice for the same caregiving hours by different public programs pay structures due to “double-dipping” rules. However, families may legally combine programs serving different purposes—for example, VA pension supplements helping the veteran while Medicaid funds three programs of separate home care hours. Disclose all funding sources to program staff.

-

Most Medicaid and VA programs require basic training, orientation, or competency checks, but not necessarily a nursing license. Training typically covers infection control, safe transfers, documentation, and emergency procedures—often 10-40 hours. Paid.care offers coaching so new caregivers feel prepared for both their role and program requirements. Respite care programs may also provide additional support.

-

If public programs aren’t available, families may use private care agreements funded by the care recipient’s income, savings, or long-term care insurance. Some nonprofits and local area agency on Aging offices offer limited stipends or respite care program vouchers. Contact your area agency on Aging or disability resource center to learn about grants and sliding-scale services for older adults. Organizations like the Family Caregiver Alliance also provide resources and guidance. While these options may not replace full income, they can reduce the overall financial strain—especially when institutional care like a nursing home or assisted living facility is not desired. States like Rhode Island, North Dakota, and South Dakota have varying support options worth exploring.