Caretakers Allowance: How Family Caregivers Can Get Paid in 2026

Key Takeaways

There is no single federal caretakers allowance in the U.S.; caregivers are paid through state Medicaid programs, VA benefits, paid family leave, long-term care insurance, and private care agreements.

In 2026, many caregivers in Indiana, Michigan, and Illinois can receive payment through Medicaid Home and Community Based Services (HCBS) and Structured Family Caregiving programs—Paid.care helps families enroll and receive weekly payments.

Typical pay ranges from $13 to $20+ per hour depending on state and program, with eligibility based on the care recipient’s medical needs and financial situation.

VA programs like the Program of Comprehensive Assistance for Family Caregivers (PCAFC) pay monthly stipends averaging $2,000–$2,800 for qualifying veterans and their caregivers.

This article walks step-by-step through each major pathway to turn unpaid caregiving into a paid job.

What Is a Caretakers Allowance?

A caretakers allowance refers to money paid to family members or friends who provide in-home personal care services for older adults or individuals with physical disabilities. This financial assistance recognizes that many caregivers sacrifice income and career advancement to support a loved one’s daily living needs.

In the United States, there is no single federal government program called a “caretakers allowance.” Instead, the term describes caregiver payments from various sources: state Medicaid programs, Veterans Affairs benefits, paid family leave laws, long-term care insurance policies, and private personal care agreements between family members.

Some countries—like the U.K. with its official Carer’s Allowance—use this phrase for a national benefit. This article focuses on U.S. options available in 2026.

Amounts and eligibility requirements vary widely by state, program type, and the health needs of the care recipient. A caregiver in California may qualify for different benefits than one in Indiana or Michigan. Technology-enabled services like Paid.care help caregivers in Indiana, Michigan, and Illinois navigate these fragmented government programs and actually get money into their bank accounts each week.

How to Get a Caretakers Allowance Through Medicaid

Medicaid is the most common source of ongoing caretaker allowance for low-income seniors and disabled adults in the U.S. in 2026. Unlike other options, Medicaid can provide indefinite funding for home care, making it the primary pathway for many caregivers seeking long-term compensation.

Medicaid operates at the state level under federal rules, which explains why program names, covered services, and pay rates differ significantly. Common structures include:

Home and Community Based Services (HCBS) waivers

Personal care services programs

Structured Family Caregiving arrangements

Consumer-directed care options

Eligibility typically depends on the care recipient meeting specific criteria:

Income below state thresholds (often 300% of SSI in many states)

Assets under limits (commonly $2,000 for individuals)

Medical necessity confirmed through assessment

Residence in the state offering the program

Many states now allow family members—including adult children, siblings, and sometimes spouses—to be hired as paid caregivers under consumer directed or self-directed options. This marks a significant shift from earlier policies that restricted payments to agency-employed aides only.

Typical hourly pay for Medicaid-funded caregivers aligns with local home care wages. In Midwestern states as of 2026, this ranges from roughly $13 to $22 per hour. Michigan’s Community Living Supports Waiver pays $15–$22 per hour equivalents, while Illinois’ Home Services Program pays relatives up to $18–$25 per hour in urban areas like Chicago.

Caregiving hours are authorized by a case manager after an in-home assessment, so your allowance amount depends on the number of approved hours per week.

Some states offer monthly stipend models rather than hourly wages. Indiana’s Structured Family Caregiving provides tiered monthly payments ranging from $1,500 to $3,500 depending on care level—assessed using tools that evaluate needs in activities of daily living like bathing, dressing, meal preparation, and medication management.

Steps to Become a Paid Caretaker Through Medicaid

Exact steps differ by state, but the overall path follows a predictable pattern. Here’s what to expect:

Confirm Medicaid status: Determine whether the care recipient is already enrolled in Medicaid or needs to apply. Contact your state Medicaid office or use an online screening tool.

Request a functional needs assessment: Ask specifically about HCBS waivers, personal care services, or similar programs. This assessment evaluates help needed with daily living activities.

Ask about consumer-directed options: Request information about self-directed or consumer directed programs that allow hiring family members as caregivers.

Complete required paperwork and training: This includes background checks, state-mandated caregiver orientation (typically 8–16 hours covering infection control, dementia care, and safety protocols), and enrollment forms.

Enroll with an approved agency or fiscal intermediary: This entity handles payroll, tax withholding, and compliance so you can receive regular monthly payments or weekly direct deposits.

As of 2026, many states require renewed assessments every 6–12 months to keep your caretaker allowance active. Missing these renewals is a common reason families lose benefits.

Caregivers must sign and submit timesheets or use an electronic visit verification (EVV) app to record hours worked. The federal 21st Century Cures Act mandates EVV compliance, and late or missing entries can delay payment significantly.

Tech-enabled services like Paid.care guide families through every step and help avoid common application process mistakes that cause 25–40% of applications to fail nationwide.

How Paid.care Helps Caregivers in Indiana, Michigan, and Illinois

If you live in Indiana, Michigan, or Illinois and are already providing unpaid care at home, Paid.care offers a practical pathway to compensation.

Paid.care helps caregivers by:

Checking eligibility: Quick online screening to determine if the care recipient may qualify for Medicaid-funded home care or specific waivers

Completing paperwork: Assistance with state forms, required documents, and coordination with state caseworkers or Area Agencies on Aging

Qualifying and training caregivers: Onboarding that meets state requirements for consumer-directed or structured family caregiving programs

Tracking hours via mobile app: EVV-compliant logging that syncs with state portals for weekly payments via direct deposit

Providing ongoing support: Care coaching and financial coaching throughout your caregiving journey

State-specific examples include:

Indiana: Structured Family Caregiving under the Family Care Waiver and Aged and Disabled Waiver

Michigan: MI Choice Waiver allowing paid family caregivers, with pay around $17–$18 per hour

Illinois: Community Care Program paying relatives approximately $19.50 per hour as personal assistants

Paid.care does not replace Medicaid but works alongside it as a service platform, reducing administrative denials by 40–50% according to internal case studies. One Michigan caregiver supporting a parent with Alzheimer’s disease transitioned from unpaid to $18/hour paid status within 45 days through Paid.care’s coordination.

Check your eligibility online in a few minutes if you live in Indiana, Michigan, or Illinois.

Veterans Affairs (VA) Caretakers Allowance Programs

The U.S. Department of Veterans Affairs offers several veterans programs that function like a caretakers allowance for an eligible veteran and their loved one’s caregiver. These programs provide financial assistance to spouses, adult children, and other family members providing ongoing in-home help.

Each program has different eligibility rules based on wartime service, disability rating, level of functional need, and where the veteran receives VA health care. Caregiver allowances may appear as higher monthly pension credit amounts, direct stipends to military caregivers, or participant-directed budgets.

Steps to Become a Paid Family Caregiver Through VA Programs

VA rules evolve, so reference 2026 guidelines from VA.gov and VA caregiver support resources. Here are the core action steps:

Confirm veteran eligibility: Verify VA health care eligibility, wartime service dates (for example, Vietnam-era service qualifies even without combat), and discharge status.

Request A&A or Housebound evaluation: If the veteran needs substantial help at home, apply for Aid and Attendance or Housebound status through VA Form 21-2680.

Apply for PCAFC: Follow the formal caregiver application process through the VA medical center. This includes clinical evaluation by peer-to-peer clinicians and required caregiver training. Approvals typically take 30–45 days.

Explore Veteran Directed Care: Ask the local VA medical center whether VDC is available in the veteran’s area. This program provides a budget that can pay family members through approved fiscal agents.

Approved primary caregivers under PCAFC receive comprehensive assistance including a monthly stipend (amount varies by geographic location and veteran’s disability rating), access to health insurance through CHAMPVA, respite care up to $2,100/month, and mental health services including counseling.

Organizations like the National Alliance for Caregiving, Family Caregiver Alliance, American Legion, and Veterans Service Officers help families interpret forms, gather evidence, and appeal denials. Denial rates average around 25%, but persistence and good record-keeping improve outcomes.

Documentation delays and missing nexus letters from physicians are common challenges. Keep copies of everything and follow up regularly.

Paid Family Leave as a Temporary Caretakers Allowance

Paid family leave provides temporary wage replacement when an employed caregiver must take unpaid leave from work to care for a seriously ill adult family member or other relative. Unlike Medicaid or VA caregiver pay, this benefit is time-limited—usually several weeks per year—based on a percentage of the worker’s usual wages.

As of 2026, 13+ states and Washington, D.C. operate paid family leave or family and medical leave insurance programs:

California (up to $1,620/week cap)

New York (up to $1,400/week)

New Jersey, Washington, Massachusetts

Colorado, Oregon, Connecticut

Minnesota, Maryland, Delaware

Rhode Island (one of the earliest adopters)

Washington’s Cares Fund, launching July 2026, provides 12 weeks at 90% wage replacement via 0.58% payroll contributions.

Eligibility is tied to the caregiver’s work history and earnings in that state—not the care recipient’s income. Benefits typically replace 60–90% of wages up to weekly caps. Many caregivers use this to bridge a gap during a health crisis before exploring longer-term options.

Federal FMLA still provides up to 12 weeks of job-protected unpaid leave, which may run concurrently with state paid leave where available.

How to Use Paid Family Leave for Caregiving

Follow these steps to access paid family leave benefits:

Check program availability: Verify whether your state and employer participate in a paid family leave program. States like North Dakota and South Dakota do not currently offer state programs.

Review family definitions: Many states include spouse, child, parent, and increasingly domestic partners, grandparents, siblings, and stepfamily member relationships.

Obtain required forms: Contact HR or check your state’s official website for application forms, filing deadlines, and medical certification requirements.

Get health care provider certification: A provider must certify that the care recipient has a serious health condition requiring the worker’s care. This may include documentation of permanent disability or chronic illness.

Submit and monitor: File the application with supporting documents. Benefits usually begin after a 7–14 day waiting period.

Paid family leave can be used intermittently in many states—for example, four hours per day over several months. Self employed workers and employees of very small businesses may need to opt in proactively, though participation rates lag at around 20% according to state audits.

Remember: paid family leave supplements but does not replace long-term caretaker allowance programs like Medicaid and VA benefits.

Long-Term Care Insurance and Personal Care Agreements

Private options differ from government benefits and aren’t available in every family—but they can be powerful tools for paying family caregivers.

Long-term care insurance (LTCI) is a policy that may pay for home health care, an assisted living facility, or nursing home care when the insured person meets “benefit triggers”—usually needing help with at least two activities of daily living or having severe cognitive impairment.

Some LTCI policies allow the policyholder to pay family caregivers, while others restrict payment to licensed home care agencies. Only 7–10 million Americans hold LTCI due to high premiums ($3,000+ annually if purchased after age 60), so this applies to a minority of families.

Personal care agreements (also called caregiver contracts) are written contracts where a care recipient agrees to pay family for care at an agreed hourly or monthly rate. When drafted correctly, these documents compensate caregivers while documenting legitimate spending for future Medicaid eligibility under 5-year look-back rules.

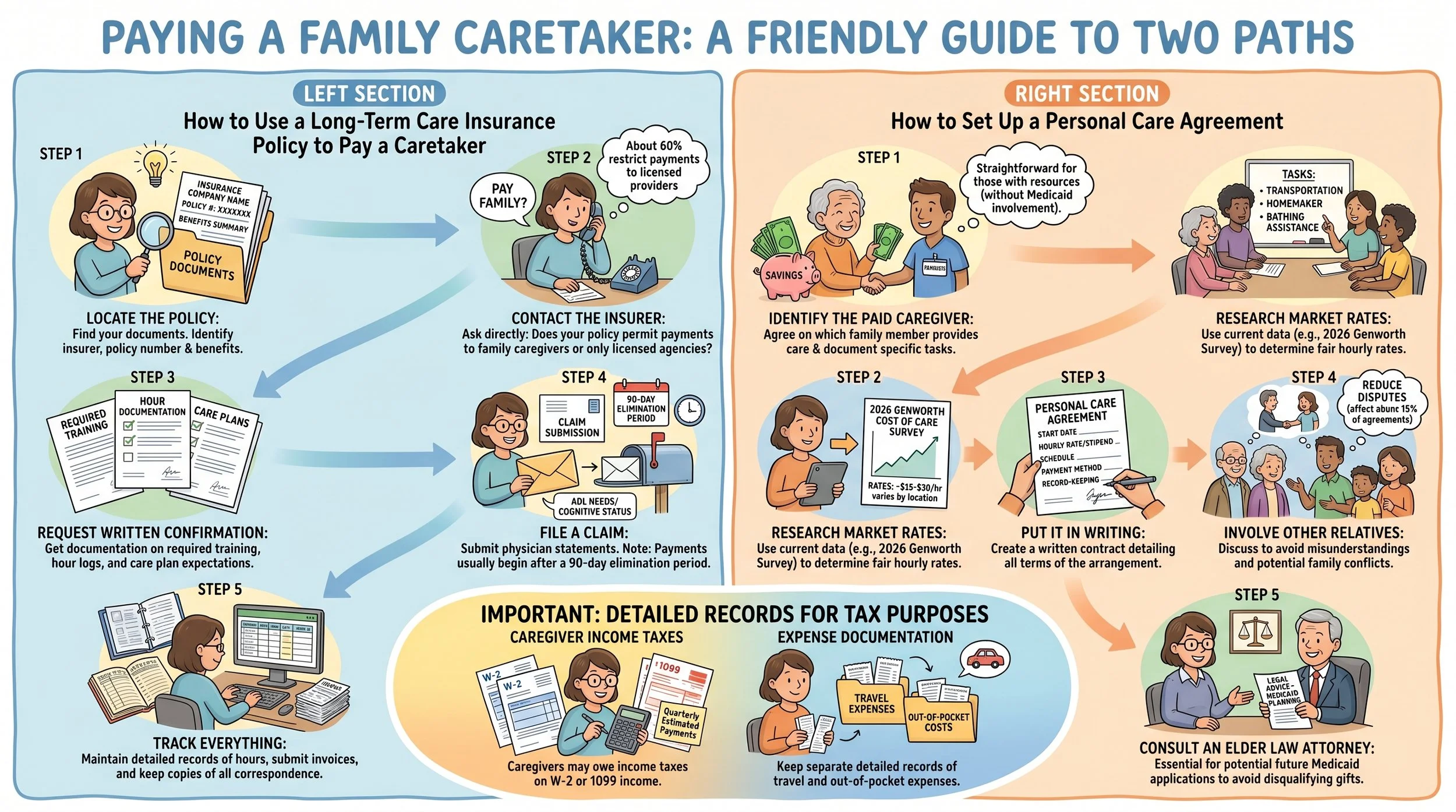

How to Use a Long-Term Care Insurance Policy to Pay a Caretaker

If your loved one has LTCI, follow these steps:

Locate the policy: Identify the insurance company, policy number, and benefits summary.

Contact the insurer: Ask directly whether the policy permits payments to family caregivers or only to licensed agencies. About 60% of policies restrict payments to licensed providers.

Request written confirmation: Get documentation of any required training, hour documentation, or care plans the insurer expects.

File a claim: When benefit triggers are met, submit physician statements about ADL needs or cognitive status. Be prepared for 90-day elimination periods before payments begin.

Track everything: Maintain detailed records of hours, submit invoices or timesheets as required, and keep copies of all correspondence.

How to Set Up a Personal Care Agreement

A personal care agreement is often the most straightforward way for a parent or relative with savings to pay family for caregiving—without Medicaid involvement.

Steps for creating one correctly:

Identify the paid caregiver: Agree on which family member will provide care and document specific tasks (transportation, homemaker services, bathing assistance, etc.).

Research market rates: Use 2026 data from care directories or local home care agencies. The Genworth Cost of Care Survey shows rates around $15–$30 per hour depending on location.

Put it in writing: Include start date, hourly rate or monthly stipend, schedule, payment method, and record-keeping requirements.

Involve other relatives: Discuss the arrangement with close family members to reduce misunderstandings and disputes (which affect about 15% of family care agreements).

Consult an elder law attorney: This is essential if the care recipient may apply for Medicaid within five years. Properly structured agreements avoid payments being treated as disqualifying gifts.

Keep detailed records of hours and payments for tax purposes. Caregivers may owe income taxes on what they receive—the IRS treats payments as taxable W-2 income requiring 1099s or quarterly estimated payments. Travel expenses and other out of pocket costs should be documented separately.

Limits of Caretakers Allowance Programs (and Why Many Caregivers Still Aren’t Paid)

Even in 2026, most U.S. informal caregivers still provide care without any formal allowance or pay. According to AARP data, 53 million family caregivers provided $600 billion in unpaid care in 2024—with only 10–15% compensated formally.

Common reasons many caregivers don’t qualify:

Income cliff: The care recipient’s income or assets are slightly too high for Medicaid but not enough to comfortably cover care costs privately

Spousal exclusion: Over 20 states (including Texas) do not allow spouses to be paid as Medicaid caregivers

VA thresholds: The veteran doesn’t meet eligibility requirements for wartime service periods or disability ratings

No paid leave law: The caregiver works in a state without paid family leave, or their employer is exempt

Limited income from work: Self employment or part-time status may affect eligibility

The patchwork of programs and complex paperwork causes eligible families to miss help they could receive. The Social Security Administration does not directly fund carer support payment programs, leaving coordination to states.

Emerging services in the caregiving space—including Paid.care—are working with state Medicaid programs, employers, and health plans to close this gap. Trends show 2026 expansions via $2.7 billion RAISE Act grants for HCBS, with 15 states expected to launch paid family leave by 2027.

Even if one path is closed, others may be available. Revisit options as laws and programs expand—your situation may qualify for financial requirements you didn’t meet previously.

How Paid.care Supports Family Caregivers Seeking a Caretakers Allowance

Paid.care operates as a tech-enabled service platform—not a government agency—focused on helping family caregivers in Indiana, Michigan, and Illinois get paid for care they are already providing to older adults or disabled persons.

Program participants in each state access different pathways:

Michigan: A caregiver helping a parent with dementia may qualify under MI Choice Waiver HCBS programs

Indiana: Structured Family Caregiving offers tiered monthly stipends based on care level

Illinois: Consumer-directed personal assistance services through the Community Care Program

Paid.care’s services work for both individual caregivers and employers seeking to support employees who have caregiving responsibilities through adult foster care navigation and eldercare locator assistance.

Start with a free online eligibility questionnaire or contact Paid.care for a consultation if you live in Indiana, Michigan, or Illinois.

FAQs

-

No single federal caretaker allowance automatically pays all family caregivers in the U.S. Instead, caregivers access payment through state Medicaid programs, VA benefits, paid family leave laws in specific states, long-term care insurance, and private care agreements. The federal government provides framework and funding for some programs, but states administer them with significant variation. Services like Paid.care help families in Indiana, Michigan, and Illinois determine which options apply to their situation.

-

Pay varies widely by program and location. Medicaid-funded in-home caregiver pay often falls in the $13–$22 per hour range in Midwestern states as of 2026. Some VA programs pay monthly stipends of $2,000–$2,800 for surviving spouses or other primary caregivers, depending on the veteran’s level of need. Personal care agreements can set any reasonable market-based rate the family can afford, though taxes still apply to all caregiver income.

-

Some Medicaid programs allow spouses to be paid caregivers, while others restrict payment to non-spouse relatives—this varies significantly by state. Certain VA programs like PCAFC do allow spouses to be designated primary caregivers and receive stipends if eligibility criteria are met. Check your state Medicaid rules and VA guidelines for 2026, or work with Paid.care or an elder law attorney to confirm what is allowed in your situation.

-

Many Medicaid and VA caregiver programs require basic training, orientation sessions, and sometimes competency checks—but not a nursing license. Training typically covers infection control, dementia care, and safety protocols, often completed online or through short in-person sessions. Even where not strictly required, training improves caregiver confidence and care quality. Paid.care coordinates required training as part of its onboarding process for program participants.

-

As of 2026, Paid.care operates primarily in Indiana, Michigan, and Illinois, with expansion to additional states planned. If you live elsewhere, use this article’s guidance to explore Medicaid waivers, VA programs, paid family leave, LTCI, and personal care agreements on your own or with local support organizations like Area Agencies on Aging. Check Paid.care’s website for the latest list of states served and sign up for updates as new regions come online.